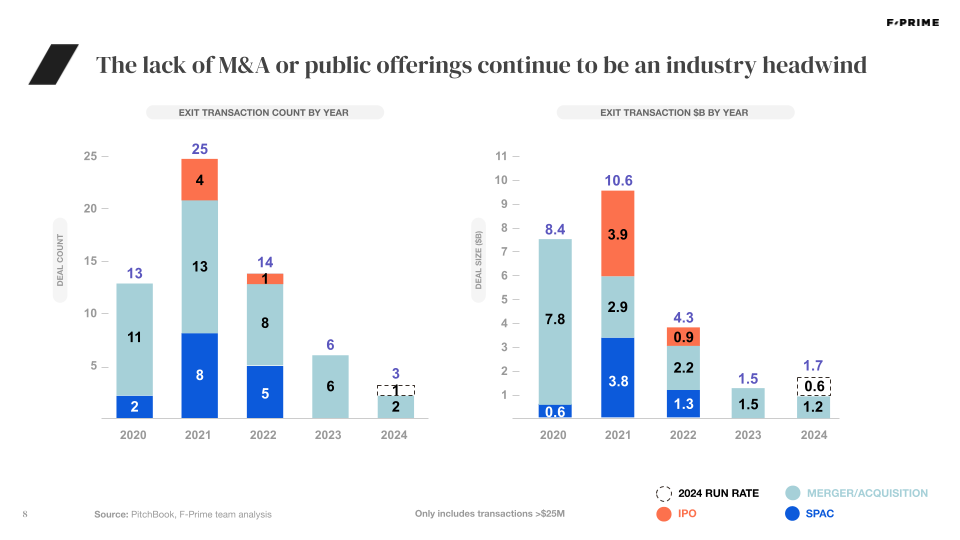

Much like the broader market, fintech IPOs have been dormant for the last three years. The sector saw a record 77 listings in 2021, but there have been very few since then.

Startups were already staying private for longer before the IPO market cooled, and one reason that may be exacerbating the freeze is that they once commanded much higher valuations in the private markets than they could hope to achieve once they open their books to public investors. Three years later, many fintechs that raised megarounds during the 2021 fintech frenzy have yet to grow into their last private market valuations.

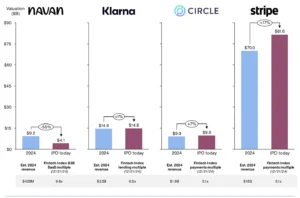

In 2025, there is hope that the fintech IPO winter is thawing. Chime, Klarna, and Navan have all confidentially filed to go public this year, and many others are considering the leap this year or next. In anticipation of this expansion of the public fintech markets, we thought it’d be fun and perhaps insightful to investigate what kind of valuation this year’s IPO candidates might reach in the public markets if they were to go public based on 2024 year-end revenue estimates. These are obviously private companies, and so our revenue estimates are made on a best-effort basis from several sources. They are not meant as investment advice, and are only meant to show where a hypothetical IPO today would put their valuations.

Navan

Last year, Navan co-founder and CEO Ariel Cohen said the company is “not far” from a public listing but that he hopes to reach profitability before then — a milestone he says is close for the business travel and expense management company. The private markets last valued the company at $9.2B with a $300M funding round in 2022, with some estimates now putting revenues in the $400M+ range.

The F-Prime Fintech Index measured B2B SaaS multiples at 9.8x by the end of Q4, meaning that if Navan were to go public today and valued similarly to its peers, it could see a $4.1B valuation — like Chime, that’s less than half of what they were once valued in the private markets.

Klarna

The Swedish fintech darling is now a BNPL leader, once valued at $45.6B in 2021 and most recently valued at $14.6B. If the most recent revenue estimates (around $2.2B) are accurate, their current EV/revenue multiple is 6.5x.

According to the F-Prime Fintech Index, Klarna’s public peers in the lending subsector traded at 6.6x at the end of Q4. So if Klarna were to go public today and valued similarly to its peers, they could see a $14.8B valuation — right in line with their last assessment by the private markets.

Circle

In October, Circle CEO Jeremy Allaire said the company is “in a financially strong position” and “very committed to the path” of going public. The company was valued at $9B last time private investors kicked the tires, and with more than $50B in reserves, some sources estimate the company is nearing $2B in revenue.

Good market comps are fuzzier for this category, but there is an argument to be made for Circle’s valuation as a payments company. Payments companies in the F-Prime Fintech Index traded at 5.1x at the end of Q4, meaning that if Circle went public today, the company could expect a public valuation of $9.6B, representing a small valuation bump over their last private market round.

Stripe

One of the most valuable private companies in the world, Stripe’s IPO may be the most anticipated over the last several years. The payments company passed the $1T total payment volume threshold in 2023, and its hypothetical public market valuation may healthily exceed its last private market valuation.

There are no perfectly reliable sources for Stripe’s revenue, but some sources estimate they surpassed $16B in 2023. Given the payments subsector’s 5.1x multiple in Q4, a version of Stripe that goes public today and reaches a similar valuation to its peers would be worth nearly $82B, a potential 17 percent premium over its last private market valuation of $70B.

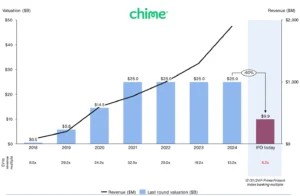

Chime

In December, Chime confidentially filed for an IPO. As one of the leading US neobanks, Chime had last raised $1B at a $25B valuation during the 2021 frenzy, commanding a multiple of more than 30x on its estimated $750M in revenue.

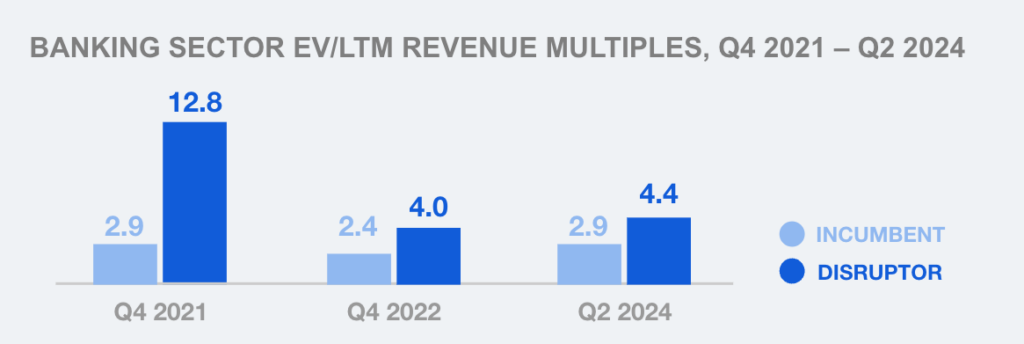

Since then, Chime has maintained a nice growth trajectory, supposedly nearing $2B in revenue by the end of 2024. However, it cannot escape the reality of banking multiples in the public markets. As you’ll see in the next section, the F-Prime Fintech Index measured banking subsector multiples at 5.2x at the end of Q4 2024. If Chime were to go public today and were valued similarly to its peers, it could see a valuation of $9.9B — less than one half of what they saw in the private markets.

By Sarah Lamont and Minesh Patel. Originally published on Fintech Prime Time.