Ashby exists to deliver a new standard of recruiting software to enable hiring excellence. It’s all-in-one recruiting platform enables high growth companies to hire more efficiently by combining features for the entire recruiting process, from sourcing to offer, with advanced analytics and automation.

Sector: Technology

For LatAm Payment Orchestration Startups, Market Fragmentation Is a Blessing in Disguise

In the vast and varied lands between Patagonia and the Rio Grande, a region entrepreneurs and investors like to call “LatAm,” there are 38 different countries using 39 different currencies.

Only 19% of Latin American adults own a credit card, and 70% of credit cards in Brazil, Argentina and Chile can’t be used internationally. Local payment methods account for 68% of online sales, and, depending on the region and merchant networks, merchants must integrate dozens of payment service providers. Meanwhile, cash voucher systems like Brazil’s boleto bancário and Mexico’s Oxxo payment network account for a significant share of Latin American consumer transactions.

Fraud is also a major problem for online merchants in Latin America. Since the onset of the pandemic, Stripe observed that fraud rates at businesses in Latin America were 97% higher than in North America and 222% higher than businesses in the Asia Pacific.

In fewer words: The payments landscape in Latin America seems hopelessly fragmented and riddled with fraud.

Meanwhile, the failure of one-click checkout startup Fast and questions about Bolt’s revenue suggest payment orchestration in the U.S. will remain dominated by the likes of Shopify and Stripe. Bolt and Fast wanted to bring Amazon’s one-click experience to all online vendors. After all, 75% of shopping carts are abandoned before payment, thanks in part to lengthy checkout processes.

But incumbents like Stripe and Adyen already dominate distribution channels, and they can easily extend a one-click solution. Meanwhile, checkout-only startups’ thin margins suffer under payment incumbents’ vertically integrated solutions, as well as from the “incentive wars” that payments, BNPL and checkout players wage on price-sensitive merchants.

So if one-click checkout startups are struggling to make headway against incumbents in the single-currency, highly digitized and concentrated U.S. market, it might seem impossible for a payment orchestration startup to succeed in the fragmented markets of Latin America.

However, we believe that fragmentation (and the absence of a Stripe-like incumbent’s dominance over the entire region) actually offers a huge opportunity for vertically integrated payments orchestration startups to capture a lot of value.

Macro tailwinds

In 2021, the number of new businesses opening Stripe accounts in Latin America rose by a whopping 518%. Even when you account for the post-COVID resurgence in business activity, that’s an unprecedented growth in opportunity for online payment providers.

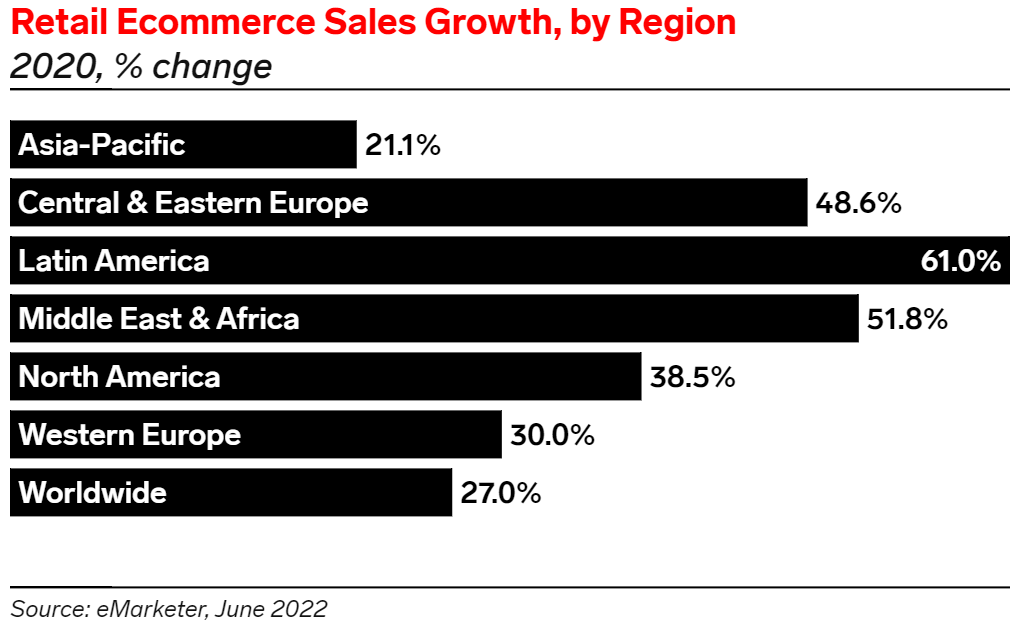

At the same time, the region’s e-commerce market is expected to reach $379 billion in 2022, representing 32% growth over 2021 and a CAGR of 25% through 2025, according to Americas Market Intelligence. That study suggests that the market will be worth $580 billion by 2024.

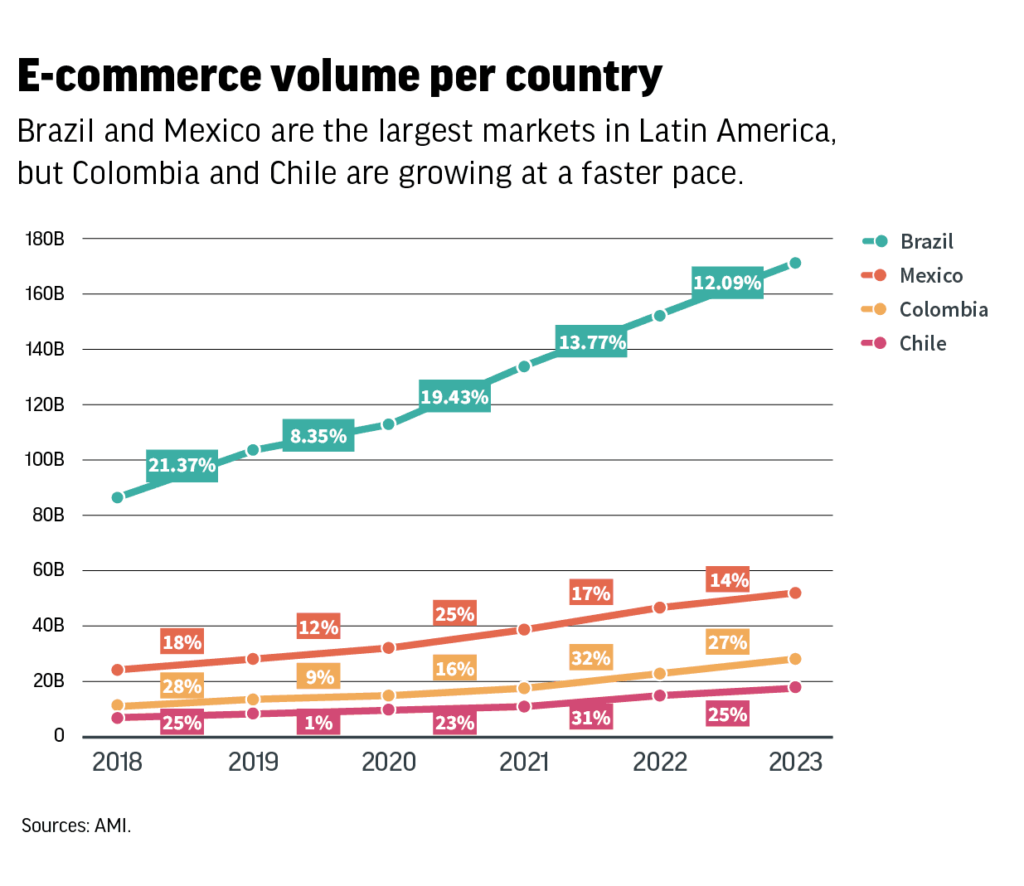

Together, Brazil and Mexico contribute about 60% of total e-commerce volume in Latin America, while Colombia and Chile are growing at a faster pace. And there’s still room for growth: Today, e-commerce only accounts for about 5% of total retail sales in LatAm.

Prerequisites for success

To be successful in Latin America, payment orchestrators must provide a robust value proposition that meets the unique conditions of the region. To help prevent payment fraud, a solution should aggregate multiple providers and data sources into a single decision engine. Balancing increasing payment acceptance rated with lowered fraud rates isn’t easy — a Stripe analysis found that the more fraud a business tries to prevent, the more likely they are to block legitimate charges in the process.

Payment orchestrators will also have to provide a single integration point for merchants, replacing the current labyrinth of local payment integrations. Smart routing technology will make switching volumes and PSPs easier and reduce costs that come with legacy acquirers and payments collectors. It would enable transaction abstraction to deliver split payments and settlement, as well as partial payments where one transaction is split across multiple sources, like vouchers and cards.

A single payment orchestrator would provide unparalleled opportunities for reporting, allowing merchants to visualize trends in payments, customers, orders and risk; understand where they can optimize; and compare their performance to peers and competitors. Third-party integrations with everything from point-of-sale and CRM platforms to rewards and loyalty programs would offer further use cases for merchants.

The current state of play

We count roughly 10 local payment orchestration players in Latin America right now and all of them are in the early stages. All approach the problem of fragmentation from a different angle, reflecting the fragmented nature of the payments landscape in the region.

For example, U.S.-based Spreedly has integrations with more than 100 payment gateway providers and third-party API endpoints worldwide. At last count, roughly 10% of its customers were based in Latin America. Meanwhile, local payments orchestrators like Plug, Tuna, Yuno, DeUna and Retry currently provide between 20 and 30 integrations.

We also have Compra Rapida and Trinio, one-click checkout startups similar to Bolt and Fast; Protego is a chargeback protection provider; Rebill has recurring billing services; and Destaxa is an offline payment orchestrator.

The technical work of building the tech and integrations in the space isn’t exactly rocket science, but working with so many merchants, acquirers, alternative payment methods, platforms and countries can feel like navigating a complex asteroid field. As a result, early exits are attractive for super payment gateway players: ZooZ sold itself to PayU in 2018; Payoneer acquired Optile in 2019; Paypal acquired GoPay in the same year; and Checkout.com took over a tiny 14-person startup called ProcessOut in 2020.

However, we believe there is an opportunity to build large, independent players in the payment orchestration space. To break out of the crowd and win the category, a successful venture would have to balance a high payment acceptance rate against low fraud and low costs and figure out the right incentives to onboard merchants with ease of product integration and configurability.

Fragmented markets like Asia, Europe and especially Latin America are more attractive than the U.S. precisely because of the heterogeneity of payment methods and currencies. While companies like Spreedly and Primer have already raised significant warchests to chase opportunities in the U.S. and Europe, the race in Latin America has just begun.

Originally published in TechCrunch. Read the full story here.

Generational Shifts Drive New Fintech Innovation and Investment

Our latest deep dive in the Wealth and Asset Management sector

Over the past few years we’ve witnessed the rapid rise of the wealth & asset management (WAM) sector. Broad media coverage of meme stocks, cryptocurrencies, and the IPOs of first-movers like Coinbase and Robinhood have heightened public attention on the work of innovative founders who are building in this space. There are now well over 3,400 startups disrupting this fintech category, yet the status quo still reigns in wealth management. As we highlighted in our inaugural State of Fintech Report, nearly 94% of annual brokerage revenue is still generated by incumbents.

The past five years have seen the largest brokerages go commission-free on trading, Robinhood surge to 7.6 million daily average revenue trades, and the rise of robo-advisors to the tune of $350 billion under management. However, the market, technology, and demographic forces that underpin our third State of Fintech sector deep-dive were set in motion years ago. And the ‘who, what, where, and how’ of wealth management have changed significantly.

In response, fintech startups are racing to manage these three dynamic forces:

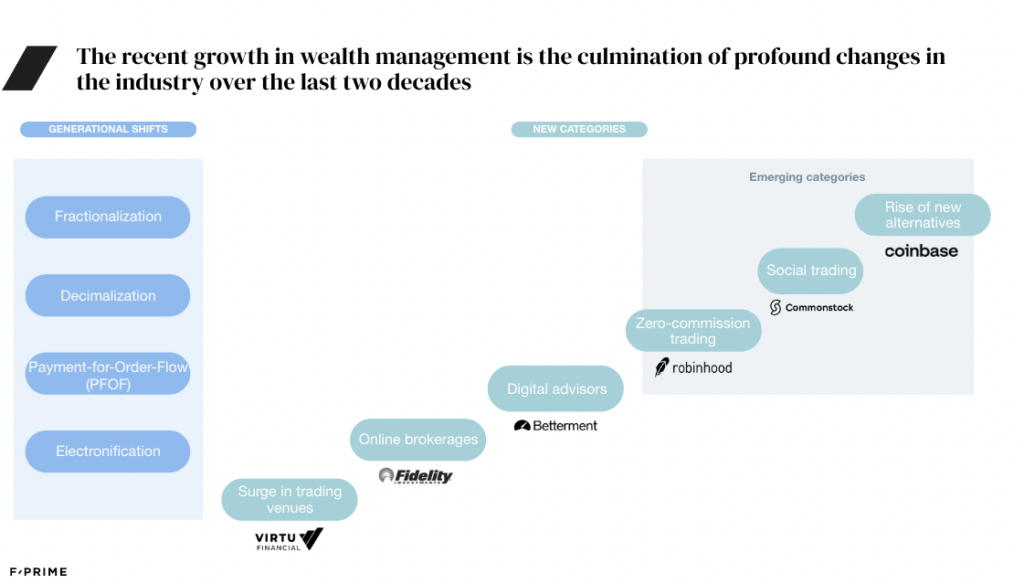

Becoming more accessible. Much of the recent growth in the wealth management ecosystem can be attributed to profound changes in the industry over the last two decades. After electronification and decimalization modernized the trading system early on, payment for order flow practices accelerated investment app development and lowered costs of trading. Most recently, fractionalization of illiquid assets has made ownership more accessible by removing hefty capital requirements.

These changes paved the way for recent advances in the industry such as commission-free trading, popularized by Robinhood during its launch in 2013. Robinhood ignited a generation by altering retail investors’ behavior with active trades, while offering a more intuitive, gamified user experience – surging to 23 million funded accounts by 2021. Similarly disruptive robo-advisors, which empower investors to automate investing and money management, are on the rise – with the top 10 robo-advisors holding an estimated $350 billion in assets under management. Lower-fee and low-touch robo-advisors are better equipped to serve populations previously underserved by traditional high-touch financial advisors.

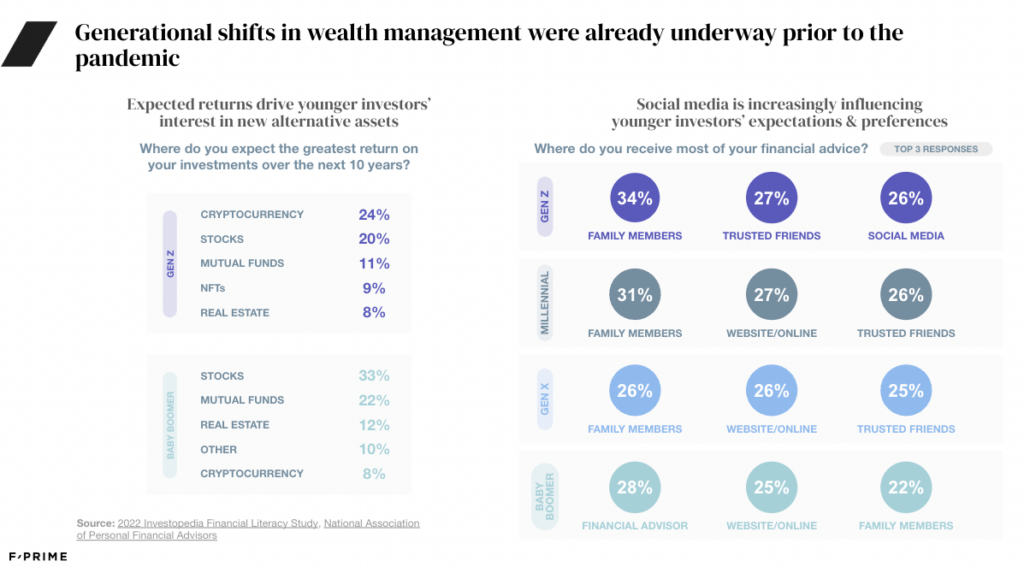

Recasting the wealth & asset management model for younger generations. As Gen Z and Millennials amass or inherit wealth, they bring a new set of expectations and preferences. Not only do younger investors more actively trade than older generations, but with longer investing time horizons, they also align their portfolios to riskier asset classes. When asked where they expect to see the greatest ROI over the next ten years, Gen Z was bullish on cryptocurrency (24% of survey respondents) while Baby Boomers were understandably more reliant upon stocks and mutual funds (33% and 22%, respectively).

Similarly, millennials and Gen Z seek advice and consume content differently than prior generations. For the first time, a generation relies heavily on social media content, including memes, to make investment decisions: 26% of Gen Z name social media as the source from which they receive most of their financial advice. On the other end of the spectrum, Baby Boomers now seek access to tools to manage wealth decumulation, assess health/wealth trade-offs, and manage extended retirements. However, having had a lifetime to accumulate wealth, their top source of financial advice continues to be traditional financial advisors (28%).

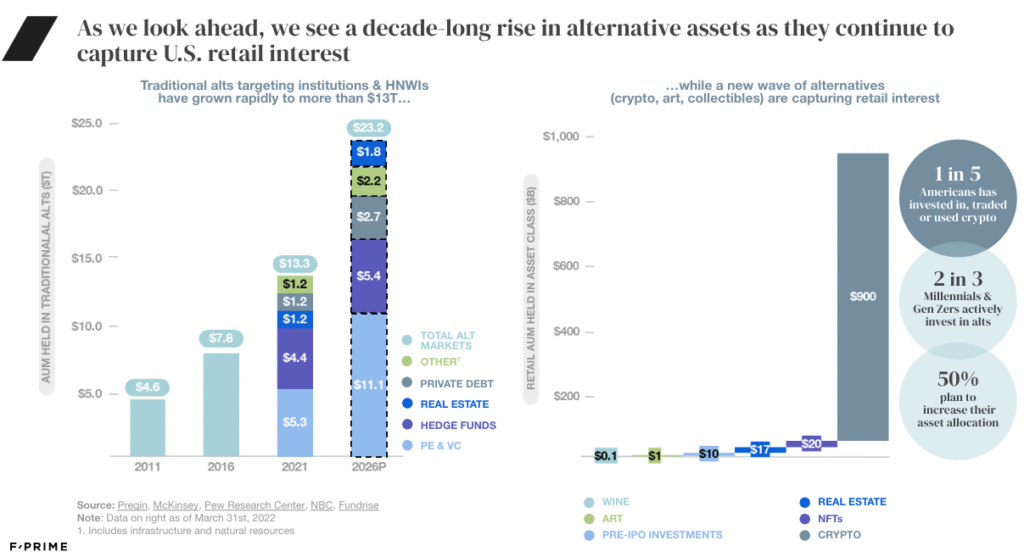

Reallocating portfolios to encompass ‘alt’ investments. Alternative assets are on the rise in two meaningful ways: traditional alts are increasing both in terms of retail access and recommended portfolio allocation, and the breadth of alternative assets is also expanding to the likes of crypto, wine, and fine art.

Historically, alts have been an exclusive domain for institutions and accredited or high net-worth individuals (with AUM nearly tripling to $12 trillion over the last decade) but are now increasingly accessible to retail investors who eschew the traditional 60/40 stock/bond split in favor of a more diversified portfolio. And not only are these ‘traditional’ alts – among them private equity/debt, hedge funds and real estate – becoming more accessible, investments in cultural assets like art, music, wine, and collectibles are rapidly growing as well. Two in three Millennials and Gen Zs invest in alts – among them crypto and NFTs – with 50% planning to increase their asset allocation in this direction.

Where in the World is Wealth and Asset Management Going?

A wave of new wealth players aim to address generational wealth and asset management shifts. Like Robinhood’s early days, many platforms have gamified the investing or savings process. Social trading platforms and ESG-focused players are addressing emerging preferences to obtain investment information from friends and influencers, as well as to focus on aligning investments with sustainability initiatives.

A historic wealth transfer (estimated at $70 trillion) is underway between the generations. Fintech startups understand this transfer presents vast opportunities to establish a high-margin niche with the fastest-growing segment of new investors, while serving older populations with retirement and wealth decumulation solutions. The market is expanding its reach to pull in younger investors and broadening to develop innovative fintech products and services that will drive growth despite today’s economic uncertainty.

The downstream impact is a deeper investment in this space. More personalized recommendations will require AI-powered advancements. More comprehensive access to alts will require a new tech stack and infrastructure. User experience must keep pace. These will remain battlefields for fintech companies, and a boon for retail investors. And the next fintech battlefields will not be limited to the U.S. – they will be global. Fintech startups are emerging to address the faster-growing global investor base in regions including LatAm, Asia, and Africa.

Latchel

Latchel is an award-winning property management technology company that empowers property managers to provide unbeatable customer experience with streamlined maintenance operations, and top-tier resident amenities. With built in layers that elevate the resident experience, property managers are also able to increase their revenue by implementing the service as a resident paid amenity. Renters get better service levels that average a 4.8/5 star rating, and property managers can increase both operational efficiency and overall profitability.

Latchel: The Operating System for Property Management

How Latchel saves property managers and owners over $1,850/unit a year

Today, there are more than 310,000 US property managers spending over 45% of their time hearing about broken toilets, calling technicians to fix chipped walls, and scheduling plumbers to unclog drains – day-to-day maintenance. Maintenance is one of the most cumbersome and tedious parts of their jobs, and Latchel aims to solve this pain point by taking over all the property management’s maintenance tasks and more. We are thrilled to be partnering with Ethan Lieber, Will Gordon, and Jullian Chavez for their $16.7M Series A as they create the new operating system for property management.

How Latchel Saves Property Managers and Owners Over $1,850/unit a Year

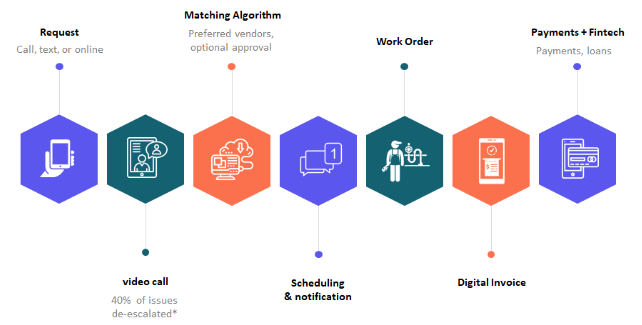

Latchel takes over all aspects of a property maintenance function. Latchel is free for property managers and charges tenants $15-18/month, similar to other utility bills. When tenants have an issue, they message Latchel, which tries to fix the issue initially over video. About 40% of maintenance issues can be solved by video without hiring a costly service professional – saving property owners 1.2 visits per tenant per year. For maintenance requests that are not resolved over video, a freelance technician is dispatched to the unit to fix the problem. A 24-hour help center is available online, over the phone, or via text, and both the tenant and property manager are able to track the progress of requests via customized dashboards. Once the job is completed, Latchel invoices the property manager and facilitates payments to the technician. The whole process saves property managers many hours a week in headache and coordination.

Tenant Maintenance Fulfillment Process

Why We Invested in Latchel

Real estate has lagged in digitization relative to other sectors, and F-Prime has been investing in all areas of proptech ranging from digital mortgage closing with SnapDocs, short-term stays with Avantstay and homeownership investment with Unison. As we surveyed the industry, we noticed the arduous process tenants and property managers go through when dealing with routine maintenance requests and once we dug into the numbers, it was immediately apparent how much value Latchel provides to property managers. On average, they see a 20% increase in revenue by switching to Latchel. Latchel is therefore able to close hefty five-figure deals that we traditionally only see with enterprise SaaS companies, while helping properties achieve 4.8/5 resident reviews. Per our analysis, helping property managers outsource maintenance is a $4B+ opportunity in the U.S.

We believe Latchel has the opportunity to become the central operating system for property management. In the coming months, we see the opportunity to layer on additional fintech and concierge products, like lending and home services, to give an even better experience to tenants, landlords, and vendors.

As part of the round, John Lin and Abdul Abdirahman will be joining the Board and John Raguin, Venture Partner and former CEO of Guidewire, will also be joining as an advisor. Thank you for welcoming F-Prime Capital as a partner in your journey!

8 Fintech VCs Discuss the Shifting Investing Landscape and How to Pitch Them in Q3 2022

The downturn has not changed our investment themes at all. We invest on five- to 10-year themes, not one to three years, and the digitization, democratization and encapsulation of financial services are only beginning.

Amid rapidly changing market conditions, TechCrunch asked eight venture capital investors about what fintech investors are looking for right now and what entrepreneurs should understand before approaching them.

Note: this story is available to TechCrunch subscribers only.

David Jegen is quoted at length in TechCrunch. Read David’s perspective here.

Teleo

Teleo is revolutionizing heavy equipment operations by turning construction and mining equipment into semi-autonomous robots. Their Teleo Supervised Autonomy technology lets contractors operate existing heavy equipment without an operator in the cab, letting a single operator control multiple pieces of equipment from a remote desk. This increases productivity, safety, and operator satisfaction — critical challenges in the construction and mining industries. Teleo is backed by UP.Partners, F-Prime Capital, K9 Ventures, YCombinator and a host of industry luminaries.

Teleo was acquired by Havoc in 2026.

The Next Wave of Autonomous Vehicles

Announcing our investment in Teleo

Six years ago, in March 2016, GM’s $500M acquisition of Cruise sparked the AV race. Within the next twelve months, Uber acquired Otto for $680M, Waymo was spun out from Google, and future unicorns Argo AI, Nuro, and Aurora were founded. Over the ensuing six years, these companies alone raised over $25 billion, and numerous other AV start-ups were launched. However, the path to autonomy has proven to be a difficult one. Despite massive capital investments, only in the last few months have Cruise and Waymo received permits to operate driverless robotaxis in select areas of San Francisco and Phoenix, though coverage areas are limited, the ride experience is more of an MVP than a fully-fledged service, and expansion to other parts of the US will take many more years.

One by-product of the excitement and technology development around autonomous vehicles has been entrepreneurs beginning to explore non-consumer use cases for AV. There are massive markets for industrial vehicles used in sectors such as construction, mining, agriculture, and logistics that are ripe for automation. Entrepreneurs have recognized that these markets are large, the value proposition for autonomy is high, and the path to success is less daunting than that for passenger vehicles.

The value proposition for industrial autonomy is compelling across many dimensions. These vehicles often operate in challenging or hazardous environments, leading to high safety risk and low operator willingness to take these jobs. Reducing reliance on human operators has obvious safety benefits and minimizes escalating costs and project delays when skilled operators are increasingly difficult to find. Technologically, the operating environment for these vehicles is more constrained and less complex than passenger roads, resulting in much faster development cycles. Also, the vehicles operate at low speed, meaning the solutions are more fault tolerant and often enable a remote, human-in-the-loop strategy to overcome issues or to deal with complex situations. The last point is particularly interesting as many of the solutions enable operators to remotely oversee multiple autonomous vehicles at a time, thus enabling people to intervene when needed to overcome complex situations, while routine tasks are automated.

We are also starting to see increased interest in the technology from leading OEMs of industrial vehicles. For example, John Deere has made 2 large acquisitions — Bear Flag Robotics (autonomous tractors) and Blue River Technology (autonomous spraying), and Caterpillar has launched an autonomous mining vehicle. The interest from OEMs is important as they are critical technology partners, they heavily influence customers and the dealer networks that are required to scale, and they help create a vibrant funding ecosystem.

At F-Prime, we are strong believers that this next wave of autonomy is ripe for investment, and we are excited to announce our most recent investment in Teleo. Teleo is targeting the mining and construction industry with an OEM-agnostic autonomous technology to retrofit contractors’ existing heavy equipment, turning them into semi-autonomous robots. The solution enables an operator to remotely oversee multiple machines from the comfort of a desk, thereby improving labor productivity, minimizing safety risk, and expanding access to these jobs. Furthermore, Teleo has seen significant interest in their solution from existing dealer networks, which they are leveraging for sales, service, and support. These dealers are highly trusted suppliers to the end customers whom they serve and are an important channel for educating the market of the value of automation.

Teleo is a great example of the next wave of AV companies, though there are many others. Burro, also an F-Prime portfolio company, is building an autonomous vehicle for transporting manually harvested row crops from the field to a packing station. This highly labor-intensive, low-skilled activity, often conducted in peak summer temperatures, is perfectly suited for automation. Fox Robotics and Third Wave Automation are building autonomous forklifts for warehouse operations. Movement of pallets in and out of trucks and around a warehouse is a significant source of labor cost in logistics centers, yet in most situations is a highly routine activity that should be automated. Electric Sheep Robotics is automating commercial lawnmowers. Commercial land maintenance is a massive market with largely routine activities which can be automated. These are just a few of the many examples, and the pace of development is only increasing. At F-Prime, we are incredibly excited to see the next wave of autonomy transform these legacy industries through higher productivity, improved safety, and greater worker satisfaction.

Silq

Silq is on a mission to bring radical visibility and real-time data from the factory floor to brands around the world, powering sourcing, manufacturing and shipping for apparel, footwear, home goods and accessory brands. Their on-site experts provide real-time updates into the production process directly from the factory floor. Paired with Silq’s proprietary technology platform, brands are able to accelerate speed-to-market and improve product quality. Customers include direct-to-consumer (DTC) and wholesale fashion and apparel brands such as Barry’s, Mightly, Mizzen+Main and Lambert in addition to design and production houses such as Pinpoint Merchandising and Stars Design Group.

Canary Technologies

Canary Technologies is modernizing the hotel tech stack, with the first mobile web end-to-end Guest Management System, digitizing everything from post-booking through checkout. Trusted by thousands of hotels in more than 65 countries, including Four Seasons, Choice Hotels, Standard Hotels and Ace Hotel Group, Canary’s solutions help hotels eliminate paper processes, boost revenue with upsells, raise staff efficiency, ensure PCI compliance, improve the guest experience, and reduce chargebacks and payment fraud.