Canoe’s mission is to unlock efficiencies in alternative investment processes by introducing purpose-built automation into the workflows of institutional investors, asset servicers, capital allocators and wealth managers.

Sector: Technology

Who Will Build the Bloomberg of Private Markets Data?

Our Series B investment in Canoe Intelligence

I recently wrote about the need for a new digital tech stack for the Alternatives fund industry. The human and paper-based workflows of venture capital, private equity, and private credit create a generational opportunity for entrepreneurs to a) digitize investor onboarding, b) modernize the back office, and c) generate an unprecedented layer of analytics-ready private fund data.

Many talented founders are building businesses to address the first two opportunities. It is still early in product execution and adoption, but startups like Flow, Entrilia, Juniper Square, +Subscribe, LemonEdge, PassThrough, Sydecar, Asset Class, and Canopy are building the future of private fund infrastructure.

The Data Problem

The data layer, however, is another matter. Fund managers almost exclusively rely on PDFs to share data with their limited partners (LPs), and there is little sign of this changing soon. We estimate that well over 100 million PDFs are sent annually, with most recipients manually entering the data into their accounting, reporting, and analytics systems.

That is too much redundant data entry, and ultimately leaves a lot of valuable data unextracted and under analyzed. Until fund managers digitize their fund operations and add APIs for data distribution, LPs are going to suffer. Players like Cambridge Associates will retain well-paid analysts to speak with fund managers, gather their data manually, and distribute benchmarks (and yes, really) through more .pdfs.

A Better Future

Now imagine a world where all private equity performance and holdings data is digital, where investors can download historical performance, review investment history, and create their own benchmarks and reporting. It is not hard to imagine because it would look like the public markets, where even Yahoo Finance has decades of analytics-ready data on nearly every equity and debt security in the world.

I anticipate three phases to this transformation. First, startups must meet the Alternatives industry where it is today – flat files like PDFs and spreadsheets. Domain-specific machine learning (ML) models can automate data extraction, classification, and normalization. While some worry that open-source ML models threaten these businesses, I see startups building defensible businesses across many industries through the thoughtful integration of open-sourced ML-models, proprietary domain-specific AI, and humans. Over time, their focus on one industry also yields a data advantage and network effect – multiple investors in the same fund using the same quarterly report, for example. Ocrolus in SMB lending, Snapdocs in mortgages, and BenchSci in pharma R&D are all good precedents.

Eventually, fund managers will modernize their accounting and fund admin, and some will distribute data digitally. This will be a great step forward. As an early investor in Quovo, I recall the initial reaction when banks did the same thing. They published APIs and told aggregators like Plaid and Quovo to use them. At first that was concerning, but aggregators quickly realized their data aggregation costs would actually decrease – while their real value-add remained. In Alternatives data, startups that have built strong customer relationships will also benefit; LPs/investors in private funds are really paying them to distribute clean, normalized data from thousands of private funds that lack common data definitions and categorizations.

And that leads to the third phase, where the leaders have the chance to become the Bloomberg of Alts data. It’s hard to believe, but there is no official “security master” for private funds, like we have for stocks and bonds. There isn’t even a common taxonomy for fund returns – I say MOIC; you say CoC. And, of course, not all funds report all metrics. With access to years of fund performance data from a broad universe of private funds, startups will have a remarkable opportunity to help investors analyze fund performance better and faster. Another exciting implication is that easily accessible alts data and analytics will lower the barrier for financial advisors and accredited investors to participate. Ultimately this is great for advisors who need to explain their recommendation to clients, and for private funds who are working to expand their investor bases.

Partnering With Canoe Intelligence to Build that Future

Abdul and I, and everyone at F-Prime Capital, are thrilled to partner with Canoe Intelligence in their pursuit of this goal. Together with Alston Zecha and Jens Neisius from our European fund Eight Roads Ventures, we led their recent Series B and are impressed with everything Canoe has accomplished already. They have a great ground game, stellar customer list, top-quartile SaaS metrics and a leading tech platform that is only getting better with scale and network effects. We have wanted to be a part of the solution in Alternatives data for many years, and we’re excited to see Canoe lead the industry. Paddle on Jason, Mike, Vishal, Michelle, Josh, Seth, Tim, and everyone on the Canoe team!

Toku

Toku is a payment orchestration company that offers a solution for collecting recurring payments in LatAm. It has three main value propositions: 1) increase payment acceptance rate via dynamic routing; 2) incur the lowest possible cost by using account-to-account payment; 3) have the best-automated payment experience.

How Startups Can Help You Win the Talent War With Tailored Employee Benefits

The employer sales channel has inherent and often overlooked advantages.

In 2021, nearly 50 million workers voluntarily left their jobs. The median tenure of employees over the age of 25 has dropped from 5.5 to 4.9 years since 2014. On average, employees 25 to 34 now stay at jobs for less than three years.

This isn’t just “quiet quitting.” U.S. workers are ready to move on from their current jobs — and they’re sending that message loud and clear.

In a story for VentureBeat, John Lin and Sarah Lamont outline how a tight labor market poses a number of opportunities for certain startups to sell their products and services as employee benefits.

Originally published in VentureBeat. Read the full story here.

What Founders Need to Know Before Selling Their Startup

The most common theme for these conversations was simply: “I wish I had known then what I know now.”

Throughout his career, David has experienced 11 different acquisitions from multiple perspectives: as a founder, an investor, and a Board member. Recently, he recently went on a listening tour to compare his experience with the post-acquisition stories of a wide range of acquired founders — and then shared his findings with Harvard Business Review.

Originally published in Harvard Business Review. Read the full story here.

Deal Engine

Deal Engine is a travel software company with a mission to bring digital transformation to the travel industry. Utilizing proprietary AI and APIs, Deal Engine brings automation to travel, eliminating manual processes, and making sure people spend their time where they generate more value.

Announcing our Investment in Deal Engine

Our latest Seed round in the travel tech space

Almost three decades into selling flights online (thanks Travelocity!), the cobweb of infrastructure that supports the travel industry has not modernized to meet the complexity growing at the surface.

Code-share agreements, ancillaries, vacation packages, layers of wholesalers, and other “business innovations” have led to booking and customer service nightmares for passengers, agencies, and airlines themselves. A simple change or refund often requires a call to customer service (have four hours to wait?) that descends into manual reading and interpretation of fare rules, calls from OTAs to airlines for clarifications, tax estimations (you’d be surprised), and other unenviable manual tasks. As important as the Global Distribution Systems (GDS’s) have been in digitizing the travel market, the pandemic highlighted the challenges the industry faces when so many of its “normal” operational processes still require human artistry to Get Stuff Done.

We believe Deal Engine, which announced its $5.3M Seed round led by F-Prime Capital today, has an opportunity to be the travel industry’s agent for digital transformation. By building a new infrastructure layer that abstracts away the complexities of fare rules and travel policies with a powerful machine-learning based engine, Deal Engine enables their partners (OTAs, TMCs, or airlines) to automate the transactions that used to be manual. The most complex changes and refunds can now be executed with a simple API call, initiated by a customer service rep or the customer themselves with the push of a button. This capability has the potential to transform the post-booking customer experience, shifting focus from cost reduction to revenue generation — all while giving the consumer the amazing experience that online travel promises.

The leadership team at Deal Engine — including Alex Jara, David Gomez-Urquiza and Isabel Carrera Quiroga — possess tremendous courage and domain expertise to tackle such a massive problem in travel. They have not been shy about bringing their disruptive solution to the behemoths we all know and sometimes love, leading Deal Engine to serve a who’s who of players in the travel industry. Betsy Mulé and I are excited to be partnering with this team, which is doing the truly hard work of making travel better for all of us.

Shout out to Thayer Ventures, PAR Capital Management, Plug and Play Tech Center and Brook Bay Capital, LLC, who also participated in the round.

Hannah Arnold

Hannah is a Venture Partner at F-Prime and leads Business Development and Mortgage at Argyle. Previously she was on F-Prime’s tech investment team focused on early-stage FinTech investments. Prior to joining F-Prime, Hannah worked closely with startups in Johannesburg as an associate with Secha Capital, where she spent every day on the ground helping teams in Secha’s portfolio scale. She was a consultant with Bain & Company in Atlanta, where she served large tech clients and worked extensively with the Private Equity practice on deals spanning healthcare, e-commerce and industrials. She began her career working for non-profits in international development, where she saw firsthand the impact that innovative financial products can have on people’s lives. Hannah received her BA in Public Policy from Duke University.

The Alternative Asset Class Needs New Infrastructure — Who Will Build It?

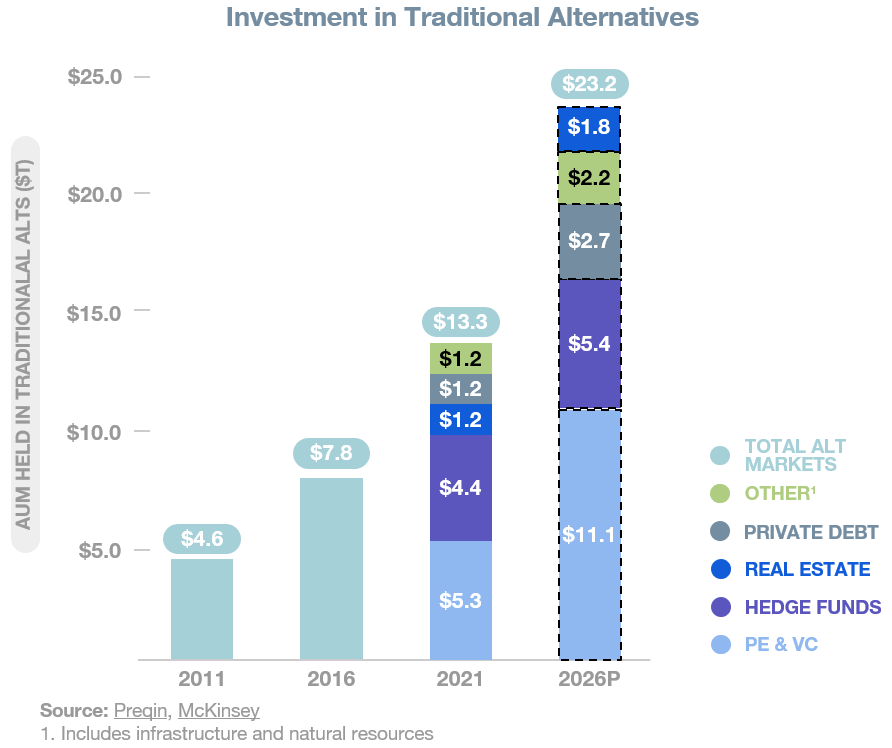

It took more than 30 years for alternative asset classes like venture capital, private equity and hedge funds to become must-have portfolio allocations, but they have finally arrived in force. Private investments in alternative assets grew to $13.3 trillion from $4.6 trillion over the 10 years ended 2021, and advisers now routinely recommend allocating 10%-25% of portfolios in these asset classes.

Liquid alternative asset classes are enjoying record inflows, and B2C-friendly distribution platforms like Moonfare, Fundrise and SeedInvest are building on-ramps for a new generation of investors.

Just as these traditional alternatives are becoming a consistent part of the modern investment portfolio, a new era of alternative assets is emerging, fueling an even broader and more fragmented landscape for investing. Dozens of platforms have launched to fractionalize, package and distribute everything from farmland, litigation finance and P2P lending to art, wine and collectibles.

Crypto added fuel to this trend and quickly became a mass-market asset category. Together with more established alternative classes like venture capital and private equity, these new alternatives give retail investors unprecedented access to asset classes that either never existed (like crypto) or were previously limited to high-net-worth investors.

However, there is a problem in alternative assets: the lack of digital infrastructure. Traditional alternative assets like venture capital and private equity at least have an ecosystem built to serve them, but that infrastructure is aging and built for a narrower base of institutional investors, like endowments, pension funds and large family offices.

As these asset classes scale and diversify their investor bases, they need a serious upgrade to modernize the fund manager/GP and investor/LP experience. The situation for emerging alternative assets is far worse. Today, investment platforms cobble together their operations — sourcing, brokerage, reporting and custody — while investors endure fragmentation throughout their journey of discovery, account creation, execution and reporting.

Let’s start with traditional alternatives

Yes, it’s oxymoronic to call alternatives “traditional,” but after more than 70 years, over $13 trillion in AUM and 10%-25% portfolio allocations, it’s hard to say that venture capital, private equity, private credit and real estate are novel forms of investment.

Investment performance for “traditional alts” is even highly correlated with public equities. The most enduring distinction is the accredited investor requirement (just 10% of the U.S. population), but Reg CF, Reg A+ and a myriad of platforms like SeedInvest and WeFunder are prying open that door as well.

As these asset classes scale, fund managers are systematically diversifying their investor bases beyond institutional investors like pension funds and endowments. The old and labor-intensive processes built around 30-year tech stacks from FIS Investran, State Street and Citco will not scale to 100,000+ financial advisers and millions of accredited investors. What’s more, the user experience is so bad, you would not want to scale it: PDFs, manual bank wires and clunky investor portals are the current “state of the art” here.

Modernizing the infrastructure for traditional alts

Fortunately, entrepreneurs are tackling the problem posed by antiquated infrastructure for traditional alternative investments.

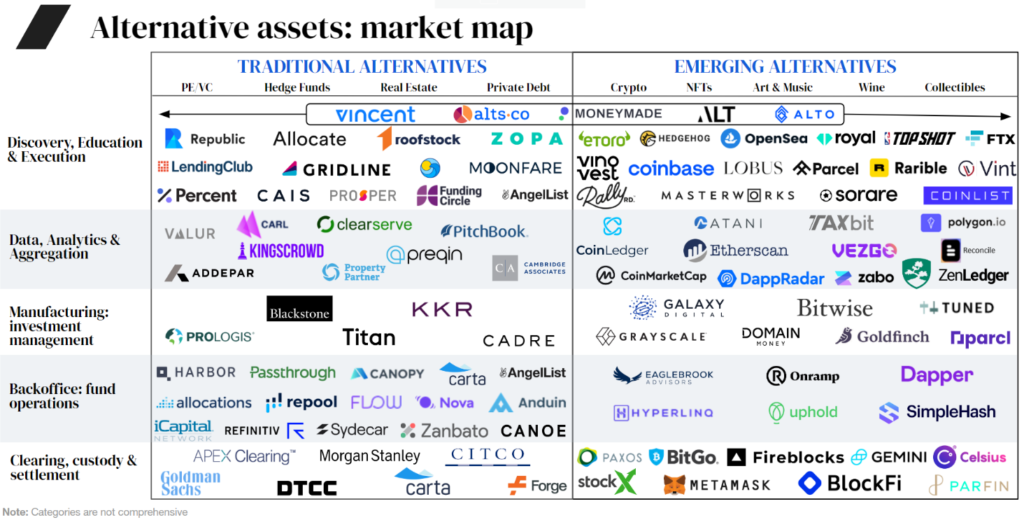

User experience: A natural entry point is the GP-to-LP (general partner to limited partner) user experience. Fundraising, LP onboarding, subscription documents, CRM and capital calls are highly visible user experiences that can be digitized and improved without touching the underlying fund infrastructure. Startups like Canopy, Flow, Asset Class and Sydecar offer delightful experiences to VC and PE fund managers and their LPs.

Back office and fund operations: For every dollar spent on the user experience, more than 5x is spent in the back office on accounting, investment monitoring and fund administration. Fund managers will not migrate off SS&C, State Street and BlackRock/eFront easily, but modernizing these processes with software that integrates external and internal resources, reduces double entry, maintains a single source of truth and automates reporting is critical to scaling.

Owning this also means a long-term sticky relationship. Aduro, Sudrania, Carta and Juniper Square have all made inroads in this backbone of the alternative asset class.

Data, analytics and aggregation: Ask an alternative asset fund manager about analytics and you’ll probably get a blank stare. That’s because LPs have long suffered quietly with their fund performance PDFs, thinking it was their responsibility to extract structured data and analyze investment performance across dozens of funds.

Tools like Addepar and Canoe Intelligence have helped, but today’s startups need to build API-first structured data models that make LP analytics a first-class citizen.

Network effects: Finally, for startups that build and execute well, there is an obvious opportunity for network effects.

Much like how Carta did this for startups and investors, we will see network effects build among GPs and LPs. Eventually, we will hear an LP ask a GP to “please use X because I already have my other fund investments there.” This position must be earned and is still likely to be winner-take-most, not all. But it is still an exciting reason for startups to build in this area.

The rise of alternatives

As traditional alternative assets have matured, a new menu of alternatives have emerged, offering all investors (retail and accredited) access to novel, fast-growing and less correlated asset classes. Some of these have always been available to wealthy investors but are now being fractionalized and virtualized to grant access to retail investors.

Examples include private credit, project finance, art, music and wine. Others, like real estate and collectibles, were already available to retail investors but are now more accessible and liquid than ever. Lastly, crypto, an asset class unto itself, has given all investors a new asset with a variety of novel and unfolding value propositions.

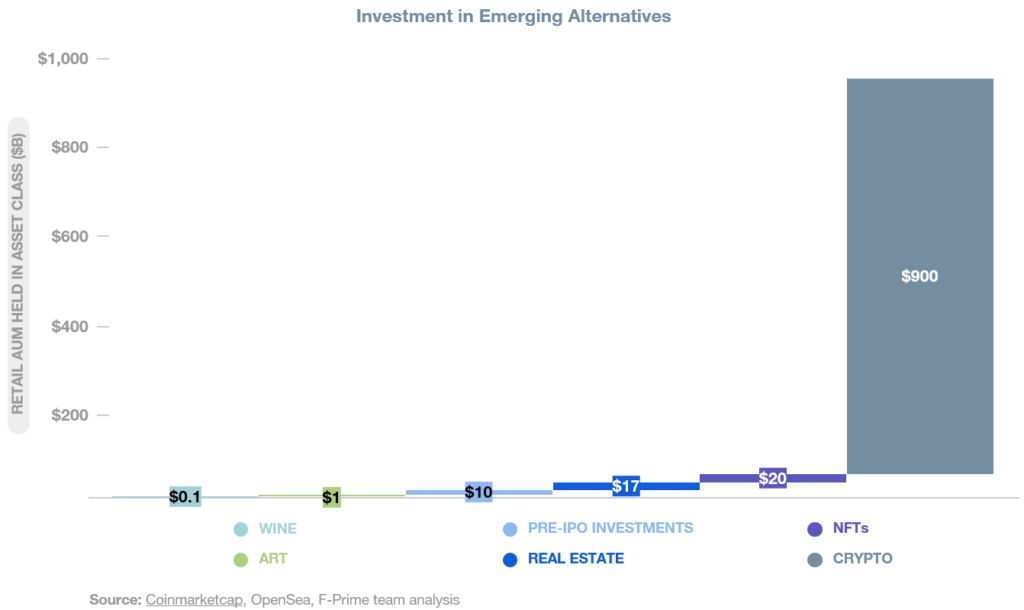

Any one of these emerging alternative assets is relatively minor, but in aggregate, they are worth about $1 trillion (despite recent sell-offs). They have attracted more than 120 million users globally and given birth to more than a 100 distribution platforms.

While they present less correlated investment return potential, another tailwind is that they tap into investors’ growing desire to have a personal connection with their investments, which could be values based or stem from intellectual curiosity. This hybrid investment-personal activity became clear with Kickstarter and Indiegogo, and these new alternative asset platforms scratch a similar itch.

The missing infrastructure for emerging alternatives

Very little of today’s infrastructure is suitable for these emerging alternative classes. Incumbent custodians like Pershing and National Financial do not custody the assets; brokerages like Charles Schwab and Morgan Stanley/E*Trade do not allow trading of these assets; financial adviser platforms like Orion and Black Diamond do not integrate with new platforms, exchanges and funds.

Consequently, investors and platforms have had to cobble together their own tools and infrastructure. Active investors can have 10 or more accounts, one for each platform on which they invest, all with separate account funding, tracking and reporting. Trading platforms have had to vertically integrate from customer acquisition to custody — think leasing secure and disaster-resistant warehouses for physical assets, or self-custody for many crypto tokens.

Here are five areas that need to be developed, and startups are beginning to go after them:

Discovery, education and execution: After a point, markets usually see aggregators emerging to tame fragmentation and provide consumers with consolidated gateways. Fidelity and Charles Schwab do that well for traditional asset classes, and players like Vincent and MoneyMade have just begun to do something similar for these newer alternative classes.

More importantly, investors need a single account from which to invest. While traditional brokerages could expand into these markets, it is more likely that an existing platform like Coinbase or one of the discovery-centric aggregators will act first and expand into a full-service, multiasset-class brokerage.

Over-the-top aggregators like LiquidFi and Stacked are headed in this direction, too, and modern retail fund structures like Titan are also positioned well.

Data, analytics and aggregation: This industry needs a Morningstar. When the mutual funds industry surged in the 1980s, Morningstar helped standardize and normalize the criteria for evaluating mutual funds. It gave retail investors confidence and financial advisers cover.

It will not be easy to do the same across so many asset types, but consistent measurements of risk, volatility, liquidity and reputation are possible. For these asset classes to scale, they will need institutional capital, actively managed funds and financial advisers — and all of these depend on better data.

Data foundations exist in some asset classes — we have Coinmetrics and Kaiko for crypto; DappRadar for NFTs; and Art Market for art — but investors need a trusted source of normalized investment metrics across all the alternative asset classes.

Investment management: Speaking of managed funds, the long-term weight of these asset classes will come from actively managed funds.

Actively managed funds account for about 80% of market capitalization in equities, and even more in fixed income, FX and commodities. Early movers like Grayscale, Galaxy and 21Shares have captured over $75 billion in AUM, and there is room for many successful players with a variety of strategies. This will be a fee-rich category.

Custody, clearing and settlement: The unsung heroes of investing are custody, clearing and settlement. Investors take them for granted in equities, debt and FX thanks to centralized institutions like the DTCC, CLS and CME, as well as the numerous incumbent financial institutions with clearing operations. Investors in the new alternatives cannot.

Investors in physical assets accept the risk that the platform they use to buy is also world class in storing and protecting their assets (also known as custody). Even when investors purchase fractionalized art or collectibles on sites like Rally or Vinovest, there is still the underlying risk of owning physical assets.

Crypto custody risks are those of self-custody (do not lose your physical storage device or private key), and if you use online brokerages like Coinbase, which do not carry SPIC insurance, your assets are not even legally yours in the event of a brokerage bankruptcy.

Clearing and settlement is better, though still fragmented with smaller custodians and transfer agents, which results in reporting and tracking complexities. The blockchain has played a valuable role in clearing and settlement for crypto and fractionalized assets, and will do so for other emerging alternative asset classes, too.

This fragmentation and lack of insurance is a natural part of an industry’s path to maturity, but to scale, we need to see diversification and consolidation right from the brokerage and execution layers through to the clearing and custody plumbing.

In the meantime, expect aggregators like MoneyMade and Stacked at least to fill the aggregation gap for investors, giving them visibility into their disparate holdings.

The opportunity for startups

Traditional alternatives are diversifying their investor base from a few thousand institutional investors to millions of accredited investors and their advisers, while an entirely new class of emerging alternative asset classes require entirely new infrastructure. Indeed, even as alternatives form a $1 trillion asset class, the sector’s platforms and their investors are cobbling together discovery data, reporting and clearing and custody where incumbent institutions have failed to step forward.

The alternative asset investment industry has never been more exciting, but it needs serious investment in new infrastructure to scale and improve the investor experience. Now is an exceptional time to build category-defining companies.

Originally published in TechCrunch. Read the full story here.

Introducing Ashby: The Data-Driven ATS

Meet the company on a mission to overhaul the applicant tracking system

My stint as acting Head of People at Juniper Square began after Thanksgiving weekend in 2019. No notice. No relevant experience to speak of.

My first task? Understand our company’s recruiting funnel and how to improve our effectiveness. I had never used our applicant tracking system (ATS) except as an interviewer. I logged in and began searching for the data and reports necessary to understand what was going on.

It took me a few hours and multiple email exchanges with customer success to realize this simply wasn’t possible. The software we called our ATS was just that — a “tracking” system — and not a reporting or operating system for this function. Data and insights are just as complex and important to recruiters as they are to sales reps, but our recruiting team was effectively operating blind.

In response, I took up an inordinate amount of our business operations team’s time by asking them to build us the dashboards we needed. We crafted a Looker instance, paid for a “data connector” add-on product charged by our ATS, but multiple months and dozens of hours later we were still wrangling data and trying to get things visible in a way that would be useful.

Since then, I’ve learned that this is an extremely common story. Ask any recruiting leader what would help them run their team more effectively, and data-driven insights will be high on that list. Today’s applicant tracking systems just don’t meet the needs of recruiting leaders.

It was around that time that I stumbled upon Ashby. After a single conversation, it was clear that this was the answer that I (and the rest of the recruiting industry) was looking for. Today, Juniper Square’s people and recruiting function is in far more capable hands than mine, and Ashby is critical to the company’s recruiting infrastructure.

An Underinvested Business Problem

At F-Prime Capital, we believe HR and People teams have been left behind by much of this generation of technology innovation, and have been fortunate to back incredible companies like Mathison, Hone, and Carrot Fertility who are working to correct this. Meanwhile, through investments like Benchling in life sciences R&D, OTA Insight in travel, and Logixboard in freight forwarding, we’ve watched software companies revolutionize industries through products with a superior ability to deliver data-driven insights. Ashby is the perfect intersection of those two themes, delivering an ATS with the data and insight recruiting teams have been missing. We’ve now been proud supporters of the company for more than two years, and are thrilled to announce our deeper partnership as lead investors of Ashby’s Series B.

Our investment thesis is quite simple: Fast-growing companies are continuing to raise the bar on talent quality, but also need to operate efficiently — especially in this time of constrained resources. This means recruiting teams are being challenged to deliver more high-quality candidates per unit of effort, and demonstrate the ROI of their work to their business partners. Being the operating system for any core business function is a recession-proof business, as the history of ATSs demonstrates.

Yesterday’s technology stack of expensive, siloed systems that lack strong reporting capabilities no longer cuts it. Ashby is a true full suite of best-in-class recruiting tools, from sourcing to scheduling, candidate management to candidate surveys, and of course, best-in-class analytics throughout the entire stack. It is the ATS of the future.

A Special Place

Having worked with the team for more than two years, my overall experience with Ashby can be summed up in two adjectives: fast and thoughtful.

Benji, Abhik, and team have assembled an incredible product development team that throws off product faster than nearly any company I’ve seen in my career. Just a few years after launching, they are quickly becoming a dominant service provider to the startup and technology community and have built better products across a wide range of recruiting business processes (sourcing, tracking, scheduling, and of course applicant tracking).

Ashby is also one of the most thoughtfully-run startups I have encountered. From their communication manifesto to their thoughts on productivity, they demonstrate that building a special company does not happen by accident, but through intention around how the work gets done.

I’m thrilled to be along for the journey. If you’re in the recruiting world, the formal launch of Ashby (not a moment too soon) coincides with today’s Series B. And even if you’re not a recruiter, keep an eye on this company — and their careers page. It’s a special place.