Abdul Abdirahman discusses our Fintech Index with Jill Maladrino on Nasdaq TradeTalks at New York Fintech Week. Abdul offers an overview of the insights that can be discovered through the index and the team’s annual State of Fintech report.

Blog posts

Abdul Abdirahman discusses our Fintech Index with Jill Maladrino on Nasdaq TradeTalks at New York Fintech Week. Abdul offers an overview of the insights that can be discovered through the index and the team’s annual State of Fintech report.

A lot of ink has been spilled speculating about FedNow, the US government’s forthcoming real-time payments infrastructure — especially how and why it differs from The Clearing House’s RTP product, same-day ACH, and Visa Direct.

However, as Rocio Wu points out in her regular column for Forbes, few have considered whether businesses and consumers in the US will actually adopt RTP payments on the back of FedNow. In this story, she compares the American payments landscape with the rest of the world, much of which has already rolled out and adopted their own government RTP infrastructure, to see what lessons can be learned.

Originally published in Forbes

Did you ever watch the original Lost in Space series from 1965?

The last 50 years of sci-fi television and movies have led many of us to expect that robots are an inevitable part of our future. To be sure, robots are now pervasive in some industries, particularly manufacturing. However, they are far from being a part of our daily lives, and the character “Robot” (of Lost in Space) still feels like a distant dream.

Nevertheless, the last few years have felt different. Autonomous vehicles are moving from research labs to the road, Boston Dynamics releases jaw-dropping new videos every few months, and (a few) venture capitalists are starting to take notice.

What’s really going on?

As one of the VCs that have actively invested in robotics the last few years, we’ve seen a rapidly changing landscape of ‘hot sectors’, business model evolution, and investment and exit dynamics. At the same time, it’s been difficult to get a grasp on exactly what’s going on. Robotics as a sector is not well-defined in the standard deal databases that VCs use, making it difficult to get a comprehensive overview.

To remedy the situation, we spent the last several months doing a comprehensive analysis of more than 1,250 robotics companies that have raised capital in the last five years, with a company-by-company analysis of which companies should be classified as ‘robotics’ and, if so, what use case they are pursuing. You can access the full report here.

Where are the VC dollars going?

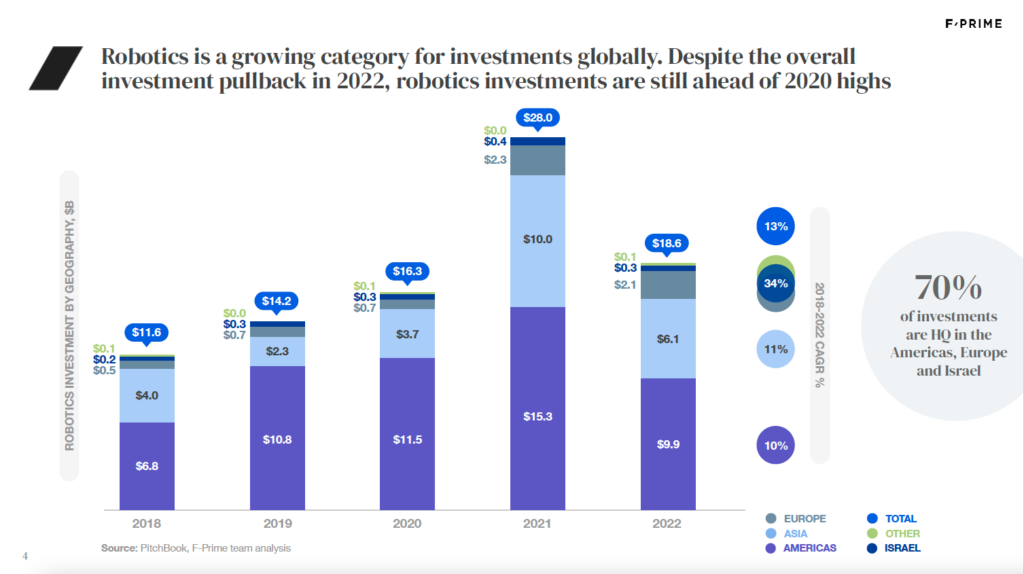

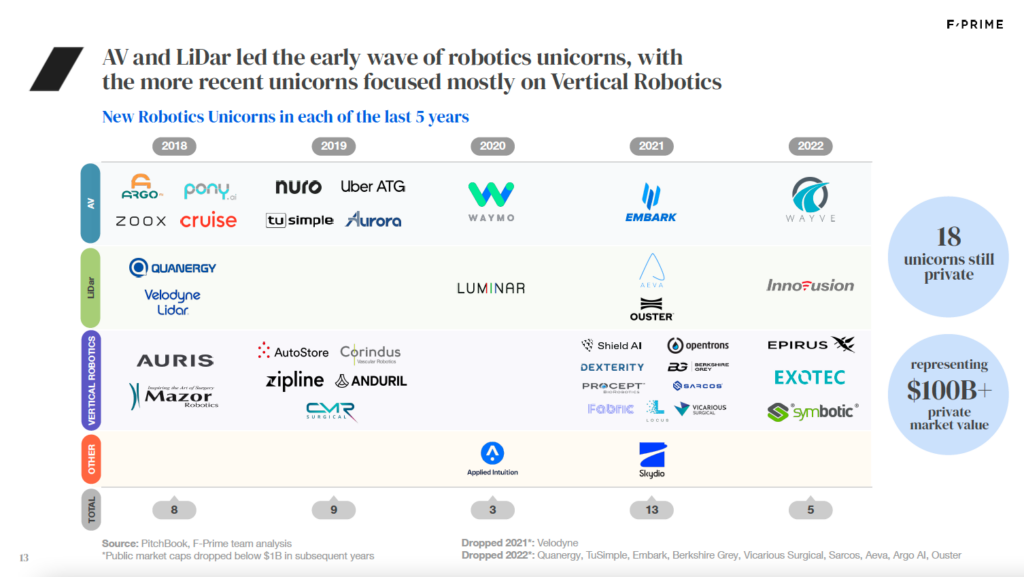

The last five years saw $90B invested in startups across the global robotics industry, representing roughly 10 percent of overall VC investments in technology. As with the rest of the market, there was a significant spike of investment in 2021, though the market remained robust into 2022, with dollars invested exceeding 2020 highs. Western markets, including the US, Europe, and Israel, were 70 percent of overall investment, though Asia — particularly China — is becoming a growing force.

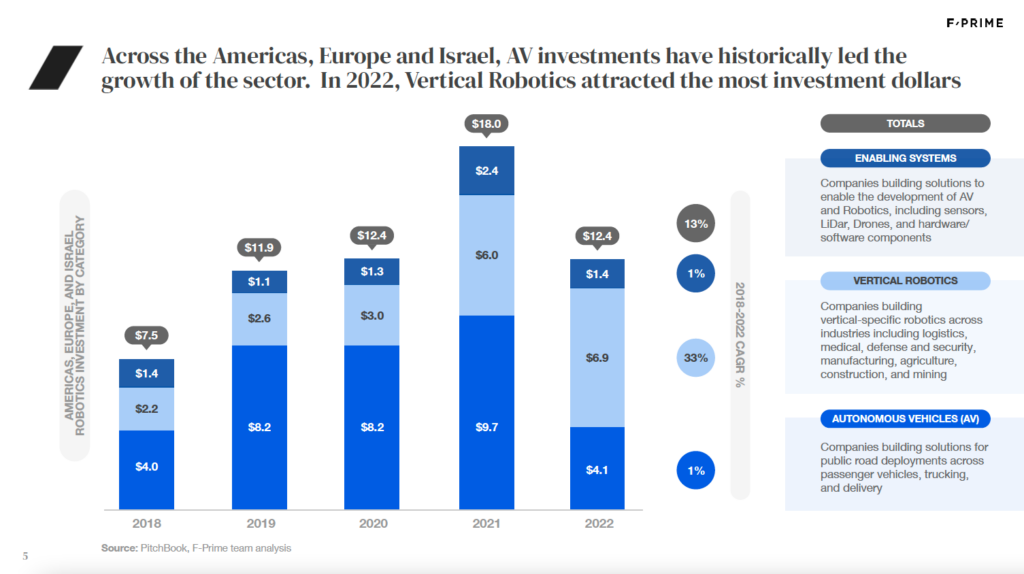

Across the Western markets, we identified three primary categories of robotics investments: Autonomous Vehicles (public roads only), Vertical Robotics (use-case specific and mostly industrial-focused – more on that below) and Enabling Systems (hardware and software components for developing a complete solution). Not surprisingly, the major driver of investment has been for AV companies, with more than 50 percent of investments flowing to AV in most years. However, with the sharp pull back of investments in 2022, AV was particularly impacted as investors began to question the path to commercialization for many of these companies.

While not a focus of our research, we expect Asia and China to play an increased role in the robotics industry. First, significant investment in technology in the region means that most sensors, robotic arms, and electronic components used in robotics will continue to be sourced from China. Furthermore, many companies in robotics — and particularly AV — are doing significant R&D work from China. Second, as robotics companies scale, China will continue to play an important role in the supply chain. While geo-political forces may change this role over time, the near-term alternatives are limited.

As an end-user market, Asia has also been an early adopter of robotics. For example, we’ve seen many companies focused on logistics robotics find success selling in Japan. Meanwhile, several Chinese automotive OEMs are already rolling out LiDar on production vehicles, while western OEMs are stuck in the planning phases. At the same time (perhaps as a reaction to geo-political tension) China is becoming a distinct ecosystem of its own for robotics. Across several use cases such as logistics, mining, and agriculture, there are a unique set of China-based players which primarily serve the local market.

You’ve heard about Vertical SaaS…what about Vertical Robotics?

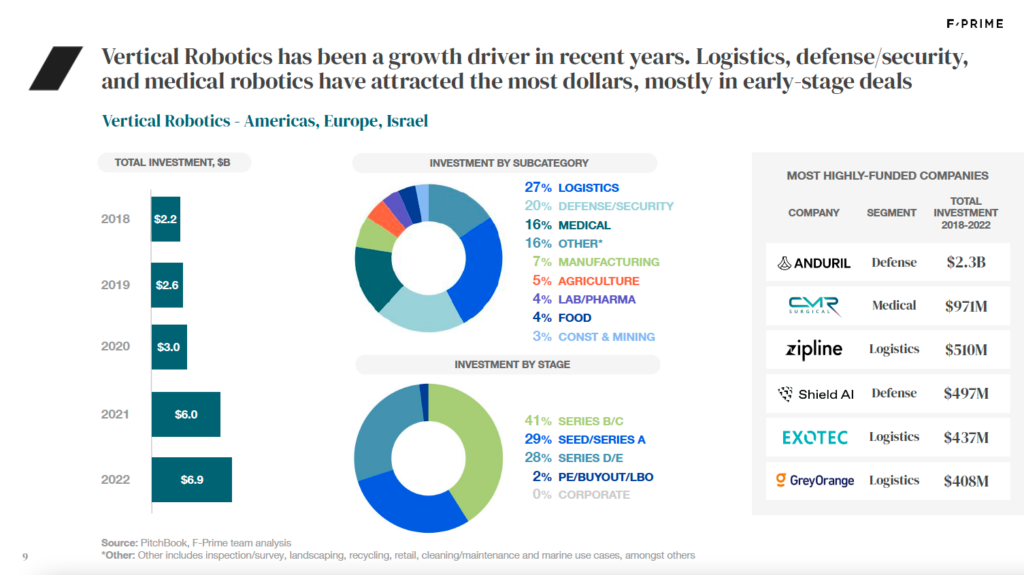

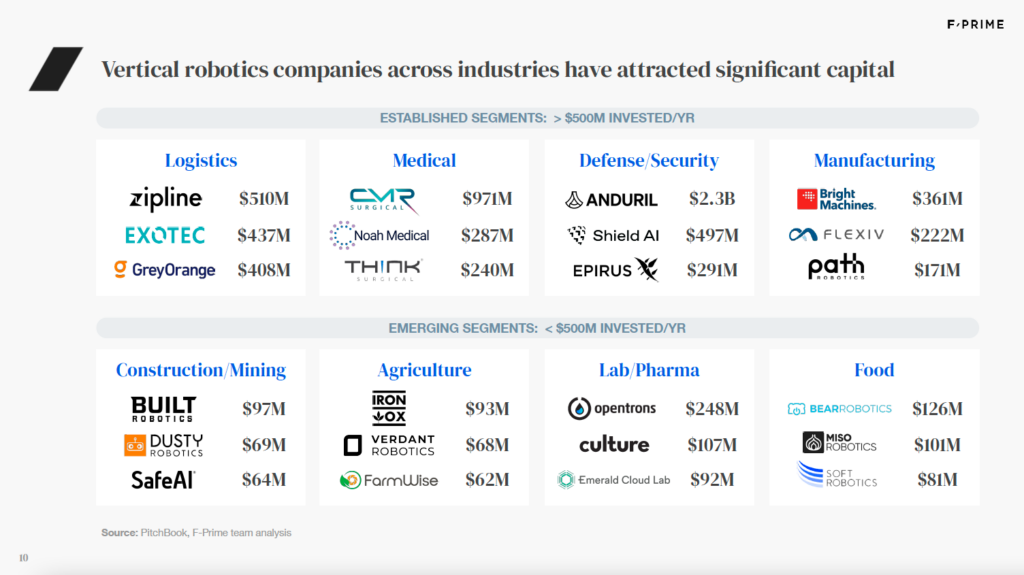

One of the more exciting trends in the industry has been the growth of Vertical Robotics, with the sector seeing significant growth in 2021 and defying the overall VC market by growing again in 2022. Vertical Robotics focuses on very specific use cases across a range of industries, including logistics, medicine, defense, and manufacturing.

Vertical Robotics is interesting for many reasons. First, companies can focus on very specific use cases within industries, bounding the problem statement to make it more suitable for robotics. Second, entrepreneurs can leverage deep domain expertise to better understand customer pain points and develop more effective go-to-market strategies. Finally, macro tailwinds of escalating labor costs and labor shortages across industries create strong willingness for customer adoption.

At the same time, Vertical Robotics is still in its infancy. Most dollars invested to-date are in early- stage deals, and other than in a few industries, the success stories are still to be told. Some areas, such as logistics, medical, and defense, have seen a disproportionate share of dollars invested and exited. Others, such as construction, mining, and agriculture, are still in the early stages of company formation and development of scalable businesses.

Is anyone making money?

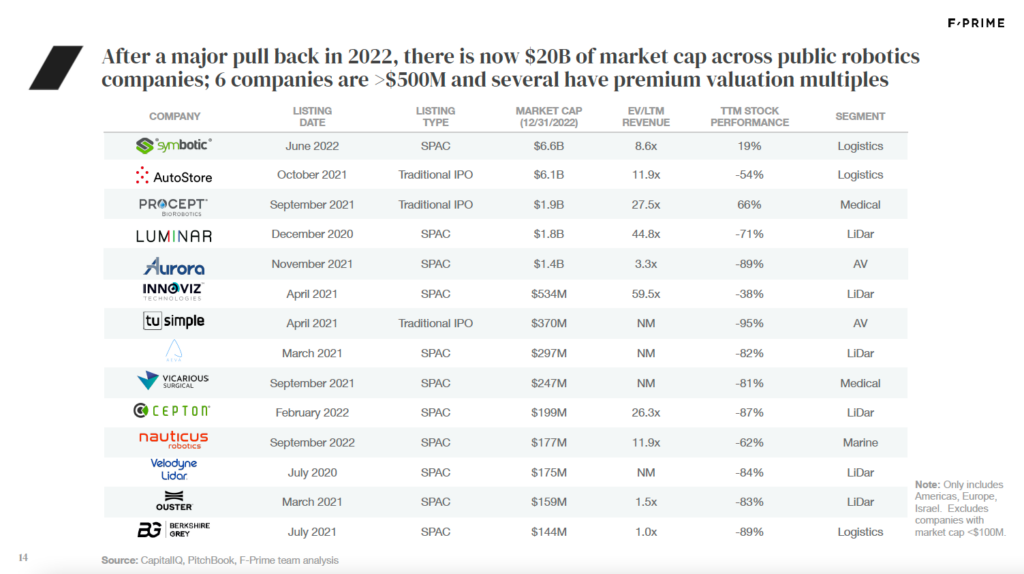

The critical sign of sustainability of any area of venture are whether dollars invested are yielding multi-fold increases in dollars exited. On this measure, while signs are positive, there is work to do. From a valuation perspective, there have been 38 robotics unicorns over the last five years. Of those, 14 had public offerings, five were acquired, one shut down (Argo), and 18 are still private.

On the public side, many companies took advantage of the SPAC frenzy in 2021, though today only three still trade above $1B market cap, and the aggregate market cap of VC-backed robotics companies which went public is only $20B. M&A has generally been more productive, with $20B of overall exit value, though it is highly skewed toward the five unicorns which were acquired. Of the 18 companies that are still private, last round valuations sum to more than $100B, though some may ultimately struggle to justify their valuations.

In total, of the $60B or so invested in western markets over the last five years, there is $140B of realized and unrealized exit value, plus upside from the earlier stage companies that are still maturing. Considering that investors own only a fraction of a company at exit, one would ideally see a multiple of at least 4-5x exit value compared to invested dollars, and as more companies mature, hopefully we will get there.

The more important exit trend for robotics may be the reversion to valuation based on business fundamentals, rather than hype. AV arguably fell into the latter camp, but Vertical Robotics feels much more like the former. Many public robotics companies trade at valuation multiples that rival those of the best SaaS companies, and a similar trend can be seen in some recent private funding rounds. In the long term, robotics exits will be driven by those companies that demonstrate the ability to scale commercially.

But hardware is hard, isn’t it?

One area of conventional VC wisdom has curtailed robotics investing: ‘never invest in hardware.’ Hardware businesses are too costly to build, product cycles are too long, and eventually they are susceptible to commoditization.

While these things continue to be true to an extent, the market is rapidly changing. Most robotics startups today rely primarily on off-the-shelf hardware, with the innovation focused on how they leverage modern advances in computer vision and machine learning. Moreover, rapid prototyping enabled by 3D printing helps create faster iteration cycles. This combination helps shorten product development times and reduce costs. At the same time, the equipment financing market is starting to warm up to venture-backed robotics companies, helping to mitigate capital requirements for production build-outs. Finally, entrepreneurs are getting more savvy about identifying use cases where robotics can deliver rapid time-to-value, and which don’t require multi-year science projects to solve.

Robotics businesses will always be ‘harder’ than building software businesses — but that also means they have a much stronger moat. Many companies have few truly direct competitors, especially when you look at Vertical Robotics start-ups. Even businesses that look similar on the surface are often solving very different use cases once you dig a layer deeper.

Danger, Will Robinson?

Investment in AV was a catalyst for a new generation of entrepreneurs and engineers to cut their teeth in robotics, and they are now leveraging that know-how to build startups that solve real customer pain points. It is true that many investors will look at the data on robotics and remain unconvinced — for them, there are too few successful exits, not enough high dollar-paying acquirers, and hardware businesses are still too hard. But the direction of travel and growing set of opportunities is unmistakable. Robotics is still in its early days as a focus sector for VCs, but the sheer breadth of activity, quality of entrepreneurs, and emergence of market leaders is starting to create a virtuous cycle.

We at F-Prime are extremely bullish about the opportunity, and we urge you to join the ride!

Meet the Chilean team that will transform payments for Latin American businesses

After publishing our thesis on payment orchestration in TechCrunch last year, we’ve come full circle: I couldn’t be more proud to announce our latest seed investment in Toku. Cristina reached out after reading our thesis, and after the first meeting we immediately fell in love with the team and the business.

Why payment orchestration?

Fragmentation: The payment landscape in LatAm is highly fragmented. 38 different countries use their own payment infrastructure and more than 39 currencies. Each country has its own card network, gateways, processors, cash, and voucher system. But we believe this fragmentation is a “blessing in disguise,” and offers a huge opportunity for payments orchestration startups.

Low Approval Rate: The payment rejection rate in LatAm is four times higher than in the US due to chargebacks, lack of funds, and ineffective fraud algorithms. Acceptance rate is as low as 30 percent in some countries.

High Fraud Rate: Stripe has reported that LatAm fraud rates are 97 percent higher than in North America, and payment acceptance rates are therefore anywhere from 30 percent in Brazil to 70 percent in Mexico.

High payment processing fees: Traditional LatAm companies do not have the 80 percent gross margins that US software companies enjoy — in fact, it’s closer to 15 percent. This means that a three percent processing fee can equal 20 percent of company margins every month. As account-to-account transfers make headway across LatAm (see Pix in Brazil, SPEI in Mexico, Transfiya in Colombia, and so on), the recurring billing value proposition will be even more attractive, faster, and cheaper, and provide a better experience.

Manual collection process: Fewer than 10 percent of active Latin American subscriptions have an automatic payment process, adding a lot of administrative burden on companies to collect payments manually every month which is prone to human errors. A lack of self-service options and cultural norms also adds to the low penetration of automatic payment processes. Subscription and recurring billing in the US are a major tailwind (we were investors in Recurly), and we believe that LatAm poses an even a bigger opportunity for a broad approach by being vertically integrated — orchestrating payments with recurring billing functionality and CRM back-office support, and so on.

A Carefree Way to Collect Recurring Revenue

Toku has become the one-stop shop for companies collecting recurring revenue in LatAm. It offers subscription management software, payment orchestration, account-to-account payments, and CRM back-office support.

The entire team is a force of nature, with best-in-class execution velocity and customer instinct. Their team culture is unparalleled, and I will never forget the night captured in the photo above when we had carne asada and sang along to guitar melodies in Toku’s home base of Santiago de Chile.

Partnering with Toku to Accelerate the Digital Transformation in LatAm

I feel incredibly fortunate to be joining the journey, particularly in the middle of Women’s History Month, of this woman-led startup in a continent where only 23 percent of funding goes to mixed-gender founding teams. Our entire team at F-Prime Capital is thrilled to partner with Toku (YC S21) to revolutionize how 50,000 businesses collect recurring revenue in LatAm. We led this seed round together with Wollef and Honey Island Capital, with other participants including existing investors FundersClub and Clocktower Technology Ventures, and individual investors such as Matias Muchnick (NotCo), Sebastian Kreis (Xepelin), Santiago Lira (Buk) and Daniel Guajardo Kushner (HealthAtom – Dentalink – Medilink). We are impressed with how the team has accomplished so much with so little. Their elegant product solution along with deep customer understanding, top-quartile SaaS metrics and exceptional execution skills — just like the bird in their new logo, the sky’s the limit for Toku.

Onward and upward Cristina Etcheberry, Francisca Noguera Astaburuaga, Enzo Tamburini Heinz, Luis Borgoño, Ignacio Errázuriz and everyone on the Toku team!

A previous wave of fintech IPOs shows us that this over-correction will be only temporary for those who do prove to be genuinely disruptive.

Originally published in Financial Revolutionist

In an op-ed for The Financial Revolutionist, Sarah Lamont describes how 2022 affected fintech companies differently across the industry’s many subsectors, outlines fintech’s revised priorities, and envisions a positive future for fintech.

Dig below the scary numbers in F-Prime’s State of Fintech 2023; there’s still plenty to be optimistic about. Fintech Nexus News sat down with John Lin to discuss the team’s findings in our latest State of Fintech Report, adding some nuance to the headline takeaways.

John Lin is quoted at length in Fintech Nexus News. Read John’s perspective here.

While it takes time for LatAm companies to mature and exit in public markets, we remain active and optimistic about the region’s startup ecosystem at the earliest stage.

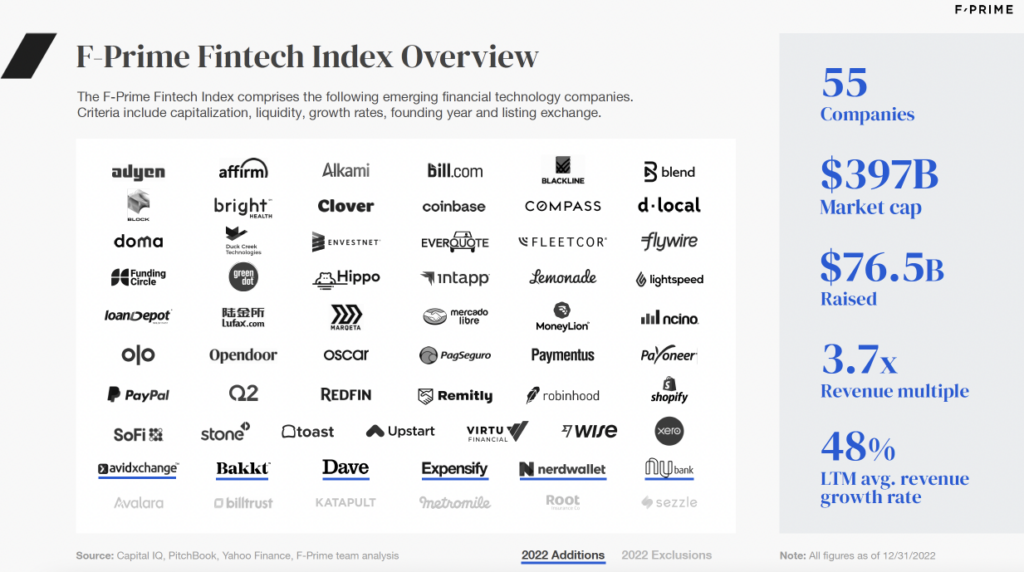

With last year’s addition of Nubank, the number of Latin American companies in the F-Prime Fintech Index grew to five, including PagSeguro, MercadoLibre, Stone, and dLocal. The F-Prime Fintech index is designed to track the performance of emerging, publicly traded financial technology companies.

In this story for LatamList, Rocio Wu discusses the year that was for public Latin American fintech companies, and their unusually strong performance relative to the broader sector in 2022.

A few words on the year ahead

For early-stage tech investors, 2022 was the year to talk about the correction in the public markets and ensure your portfolio companies had 18-24 months of runway. As we approach the end of that runway, the realities of over-funding and over-spending are setting in.

I lived the dot-com and 2008 corrections, and unfortunately 2023 is bound to be an incredibly challenging and unpleasant year for founders, tech employees, and investors.

Many private companies will be just fine. Indeed, one thing that separates the last decade from the dot-com era is the fundamentally high quality of today’s business models. The roots of today’s crisis owe more to excess capital and unconstrained spending.

We are going to see four scenarios return that were largely absent for the last 10 years.

I’ve seen examples of them all over the last 60 days.

1. The quiet wind down. Startups that cannot raise sufficient capital at any valuation are shutting down and sending heartfelt thank you emails to their customers. Sadly, these won’t always be “bad businesses,” but for a variety of reasons – team, lack of traction, out-of-favor sector, down-rounds that are simply too draconian — investors just will not invest more capital (despite all the “dry-powder”).

2. The strong(er) acquire the weak(er). Every well-capitalized and scaled startup ($50M+ revenue) is drafting a list of target acquisitions. Every poorly capitalized, but semi-scaled startup has a list of acquirers. While there will be a lot of talking, the targets will rarely get “fair value” because acquirers have so many choices and will view every acquisition opportunistically – if they can’t get a good asset at a great price, they will move on to the next.

Valuing businesses is itself a challenge, especially when everyone knows the last-round valuation was too high. Investors and founders will opt for simple heuristics like exchange ratios based on ARR or gross profit. In reality, there is not much value in building discounted cash flow models (DCFs), but the target will struggle to capture value if it’s growing two or three times faster than the acquirer. Exchange ratios do not, but if the target is lucky, it can get a higher multiple on their ARR or gross profit than on the acquirer’s, to reflect that growth differential. Unfortunately, in this environment that will rarely happen.

3. VCs play match makers. Investors will catalyze business combinations for good reasons – gaining scale while reducing competition – and for bad reasons — one problem portfolio company is better than two. Obviously, founders should be leery of the latter and evaluate the M&A on its merits.

4. Recaps return. Recaps are down-rounds with bombs attached. They target two problems – co-investors who won’t or can’t invest more capital, and management teams that will need more equity to be incentivized following the down-round. With pay-to-play and pull-through provisions, early investors will suffer major dilution and/or lose preferred stock rights if they do not invest more capital.

Recaps are appearing and they will be contagious. Investors who have been subject to them in one portfolio company will introduce them at another. And as investors invest more capital than they had reserved to protect their earlier investments, they will shift reserves from one company to another inducing the vicious cycle. Fortunately, founders of fundamentally good businesses can come out OK with post-round equity top-ups, but there will be a lot of collateral damage.

While these will be challenging times for many startups, being aware of these scenarios and approaching them proactively and with the right mindset will help founders and investors alike. Great businesses continue to founded, disruption will continue, and a lot of investor capital is available for the future.

Last year was the calm before the storm for private fintech companies, so we are going to see a lot of market consolidation this year.

Rocio Wu discusses our State of Fintech Report with Jill Maladrino on Nasdaq TradeTalks, covering how investors weighed the growth potential in the fintech sector in 2022, how they’re being valued now, and what investors can expect in 2023.

Originally published by Nasdaq TradeTalks

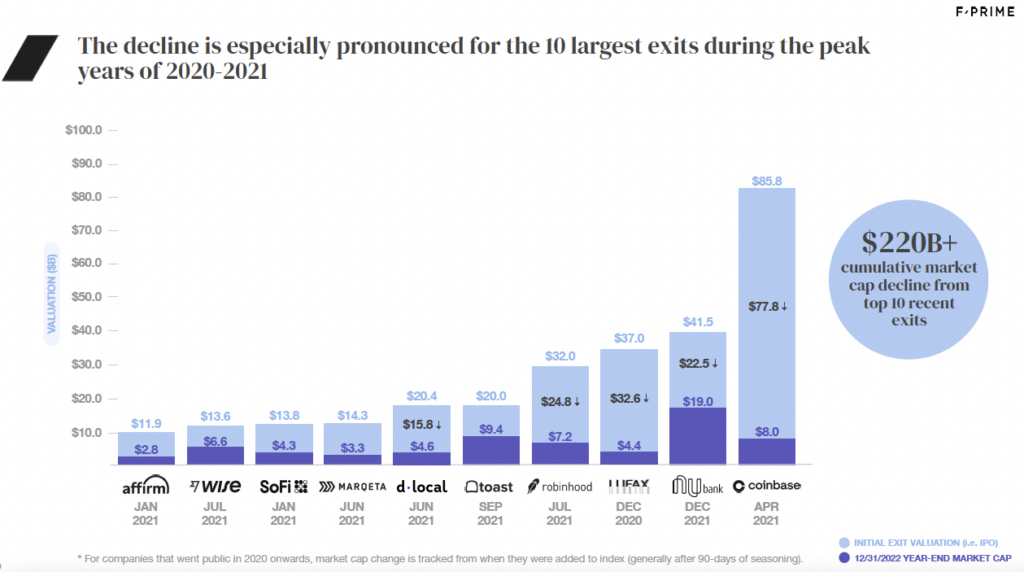

Fintech was on fire in 2021. A record 77 fintech companies went public, which included eight of the largest 10 exits in history.

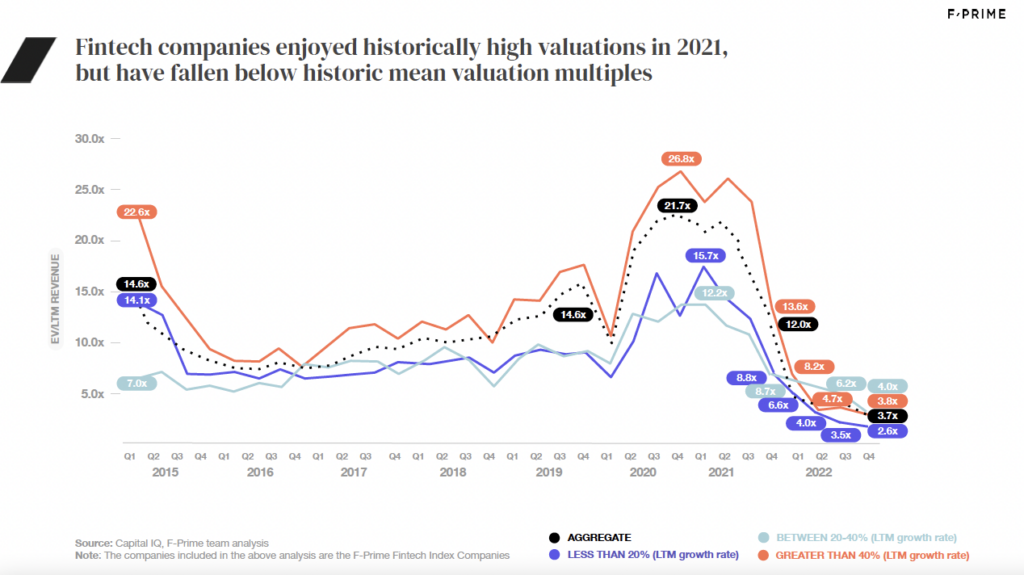

However, in 2022 public investors re-appraised many fintech companies, prioritizing capital efficiency and shifting valuation multiples to align more closely with traditional financial services businesses. The F-Prime Fintech Index declined 72% over the course of 2022. Rising interest rates and macroeconomic uncertainty added to the significant valuation declines with certain fintech verticals seeing larger declines. Despite the drop in valuations, fintech disruptors grew rapidly, continued to capture market share, and give venture investors many reasons for long-term optimism.

New Logos in the Fintech Index

The average company in the Fintech Index lost 56% of its value in 2022. Companies that listed between 2020 and 2022 — two thirds of the companies in the Fintech Index — fared even worse, falling 65%. Because the IPO market came to a halt in 2022, there were few additions to the Index. Of the six new companies added to the Index last year, only Dave went public in 2022. The others — AvidXchange, Bakkt, Expensify, NerdWallet, and Nubank — all went public in Q4 of 2021 and, per our methodology, required 90 days to “season” before we added them to the Index.

We also saw three acquisitions of Fintech Index companies in 2022. Metromile was acquired by Lemonade, Vista Equity Partners took Avalara private, and EQT Private Equity did the same with Billtrust. Meanwhile, Katapult, Root Insurance, and Sezzle failed to meet the criteria to remain on the Fintech Index, and were therefore removed at the end of 2022.

Variation Across Verticals

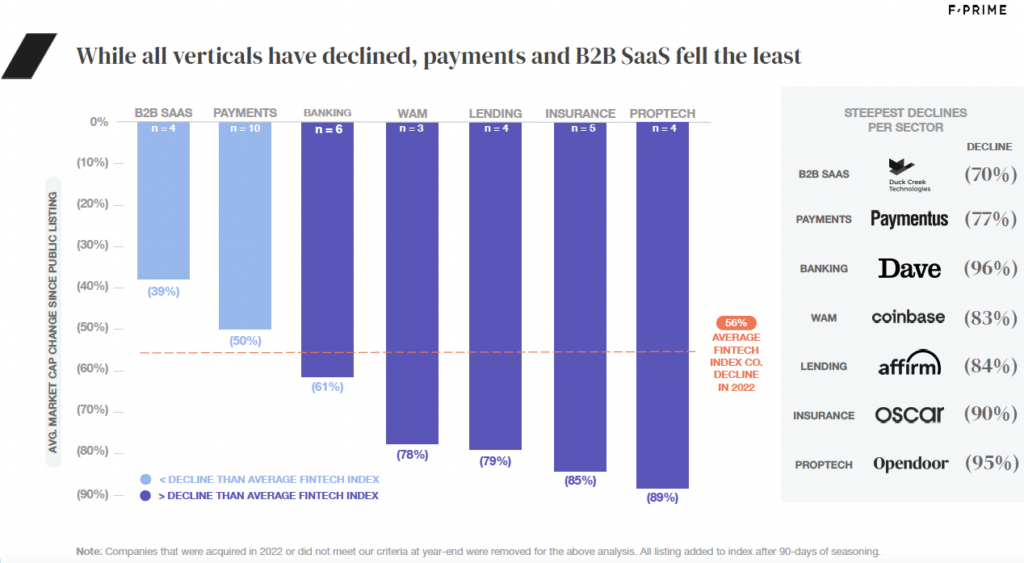

While nearly all tech and fintech stocks fell in 2022, the Fintech Index reveals meaningful differences across fintech verticals. We saw the steepest valuation declines in proptech, insurance, lending, and wealth/asset management — verticals that are especially exposed to rising interest rates and thin liquidity markets. Unsurprisingly, B2B fintech and payment companies saw less than average declines.

Fintech Index companies that went public in or after 2020 exited at a peak market, leaving them vulnerable to significant losses in the next downturn. Companies like Coinbase saw a 90% decline in market cap over the course of 2022.

Some of those corrections appear to revert company valuations to historical norms. Others are especially large, with multiples significantly below historical averages as public markets begin to distinguish tech-enabled versions of existing financial institutions from truly disruptive approaches to financial services.

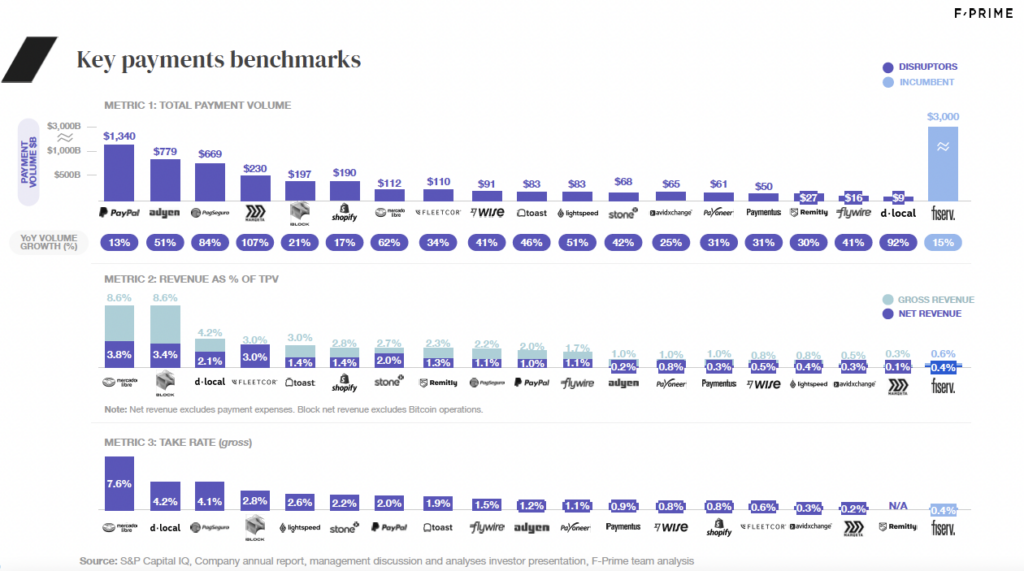

New Metrics to Capture a Diverse Sector

Compared to SaaS companies, fintech business models vary greatly across verticals. Thus, we need to evaluate the diverse set of companies within each fintech vertical distinctively. In response, we are adding new vertical specific metrics to the Fintech Index so they may serve as a quick reference for founders, investors and others to benchmark against recently listed public disruptors and incumbents in the financial services sector.

In its current state, the Fintech Index can highlight top-performing companies in each category, however over the coming months we will roll out dynamic charts showcasing key benchmarks across fintech verticals.

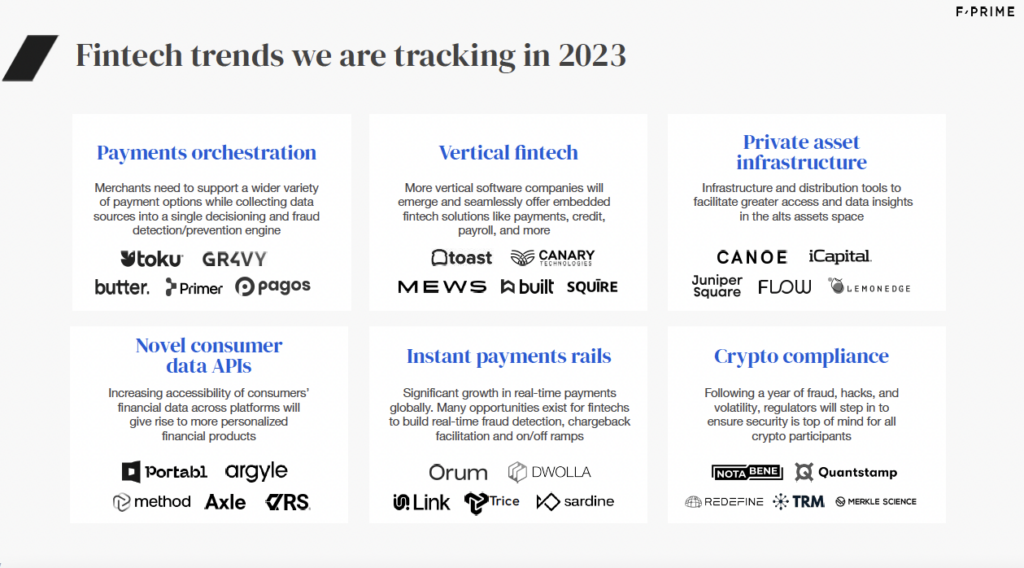

The Year Ahead

We’re tracking a number of disruptive trends across all fintech verticals, however below are some of the areas we are particularly excited about in 2023:

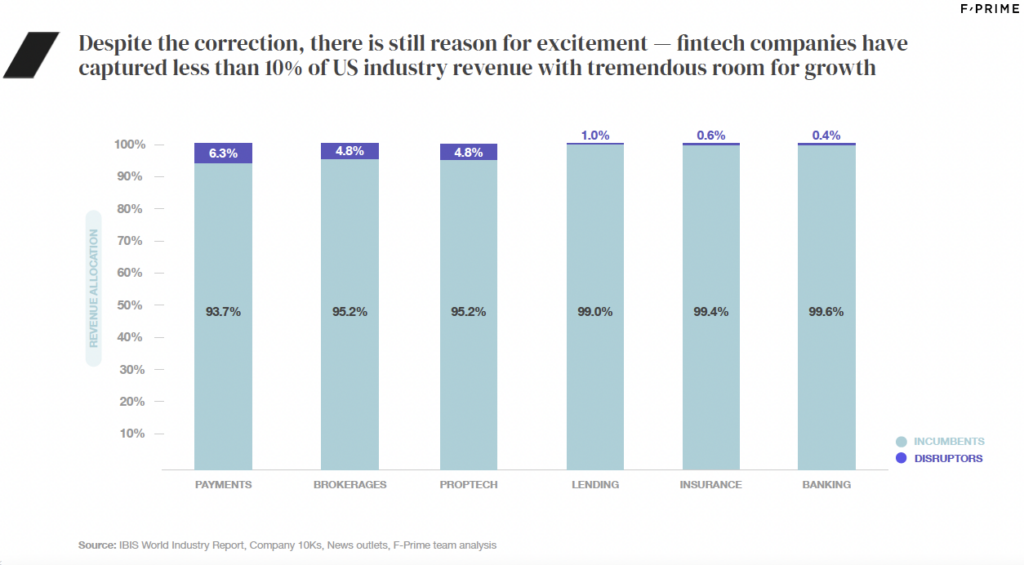

While 2022 was a tough year for fintech, we remain steadfast in our conviction that this is a great category to build and invest in. For one, fintechs are still in the early innings of capturing financial services revenue share — right now, fintech companies have captured approximately five percent of total financial services industry revenue.

Meanwhile, fintech continues to eat the world as the embedding of fintech products accelerates across new verticals. As early backers of Toast and Flywire, we saw this first-hand in the restaurant industry and higher education. We see this in other verticals where disruptors like Shopify, ServiceTitan, Procore, Mindbody, and others are doing the same. Embedded fintech not only centralizes and improves the experience for users — it also increases TAM and makes previously overlooked verticals more interesting as ARPU/ACVs can increase 2–5x.

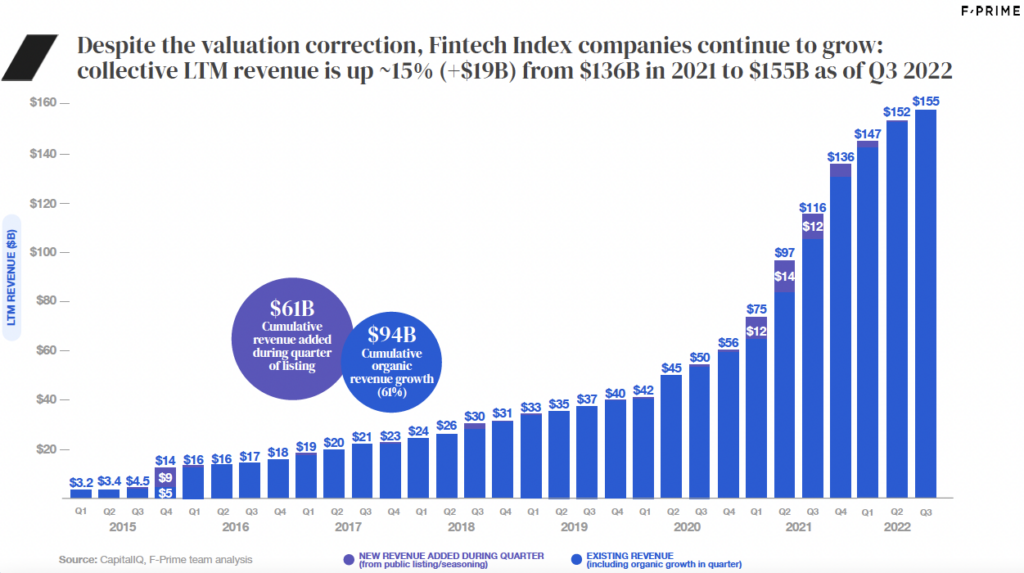

Finally, disruptors are both growing the pie and taking market share from incumbents. In the first three quarters of 2022, Fintech Index companies grew revenue 45%+ on average, and added $19 billion in revenue collectively to the Index. Furthermore, the vast majority of that growth was organic, as no new companies were added to the Index after Q1 2022.

We also expect M&A to pick up dramatically in 2023 and especially in 2024, as buyers and sellers find valuation alignment. As mentioned earlier, private equity firms have increased their acquisitions of Fintech Index companies and we expect more buyout transactions — for example, DuckCreek is due to be acquired by Vista Equity Partners in 2023. We will remove the company from the Index once the transaction closes, as we did with the three aforementioned acquisitions in 2022.

Beyond that, we encourage you to dive into the report and join us on Thursday March 9th for an online discussion of its findings with the F-Prime team. What do you think of our conclusions? How excited are you for those new dynamic metrics to drop? And what are you most looking forward to in fintech-land in 2023? Drop us a line on Twitter and LinkedIn — and if you’re building or investing in fintech, let’s connect!