Burro is a robotics company building an autonomous platform designed to free growers and their workforce from tedious tasks, while building the modular base for greater autonomy. Founded in 2017, the company offers the only fully autonomous, plug-and-play collaborative farming robot on the market.

Sector: Technology

Guros

Guros is an embedded insurance company in Mexico that’s transforming the entire insurance experience, from purchasing to managing vehicle and mobile insurance. They’re on a mission to democratize insurance in Latin America; both for end-customers and neobanks/fintechs who want to embed insurance into their platform, but need to do so in a much simpler, faster, and reliable way.

Warmly,

Warmly is the first AI-fueled pipeline acceleration platform that harnesses the power of existing sales enablement and intent tools to automatically identify high propensity website visitors and alert them to sales for real-time engagement. It’s the first such solution purpose built to meet the business and budget needs of SMBs.

These Startups Are Helping Employers Prepare for the Post-COVID Workplace

In our post-pandemic lives, we will likely never return to the full level of in-person engagements we relied on before COVID broke out.

Summer is upon us, almost half of America’s adult population is fully vaccinated, and, increasingly, employers are beginning to plan to welcome employees back to the office. Employers are facing a complex new reality in which only some employees return to the office some of the time. As employers prepare for the post-COVID workplace, startups are creating tools to help them establish new work routines that accommodate distributed workforces and leverage our newfound reliance on video.

In a story for VentureBeat, John Lin outlines the post-COVID workplace trends he finds particularly exciting.

Originally published in VentureBeat. Read the full story here.

Healthcare is the next wave of data liberation

At F-Prime, we have been closely involved in the liberation of financial, to the benefit of service providers and consumers alike. In this story for TechCrunch, Carl Byers and David Jegen reflect on how while the winners in healthcare data transformation will look different than they did in the realm of fintech, even as the industry heads toward a similar end state.

Originally published in TechCrunch. Read the full story here.

1upHealth

1upHealth provides data interoperability between healthcare systems at a very low cost, fractions of a cent per API call, utilizing the latest FHIR® standards, and patient-authorized access, to ensure the best insights at the lowest costs across healthcare providers for low-income, diverse, and vulnerable populations.

Betsy Mulé

Betsy Mulé is a Principal at F-Prime, where she focuses on early-stage investments in enterprise technology and robotics. Prior to joining F-Prime, she was a strategy consultant at Mars & Co. where she advised Fortune 500 companies across the US, LatAm and Europe.

Betsy is a graduate of MIT where she majored in Chemical-Biological Engineering.

ConnexPay

ConnexPay is revolutionizing the payment distribution process by offering a combined merchant acquiring and virtual card issuing solution for mid-sized companies. The company’s technology simplifies an antiquated workflow, eliminates the need for pre-funded accounts, reduces supplier risk and the cost of accepting card payments while safeguarding consumer spend. Backed by F-Prime Capital and BIP Capital, ConnexPay is becoming the industry leader in payments for industries historically viewed as high risk to payment providers.

Announcing our Investment in ConnexPay

Managing payments on behalf of their customers is essential to powering the best customer experience possible.

If you’ve ever purchased a trip with Booking.com, a gift from Etsy, or insurance from an agent, you’ve experienced the critical role that brokers, agents, marketplaces, and other intermediaries play in our society. Far from being simply middlemen, these intermediaries own the customer relationship and more importantly customer experience, providing essential value to customers such as a brand they trust, price comparison, product recommendation, or simply coordination across multiple parties to simplify the purchase experience.

These groups are massive contributors to the economy — travel agents, freight brokers, and insurance agents alone control over $1.5T of spend in the U.S. — and yet their customer experience often falls short when it comes to managing payments. Right at the point of purchasing, many intermediaries are forced to turn over the customer to the party providing the product or service (e.g. a travel agent passing your credit card details to the hotel or airline for processing), sacrificing control of the customer payment experience at the most critical time and losing the ability to manage refunds, chargebacks or ongoing purchase updates thereafter.

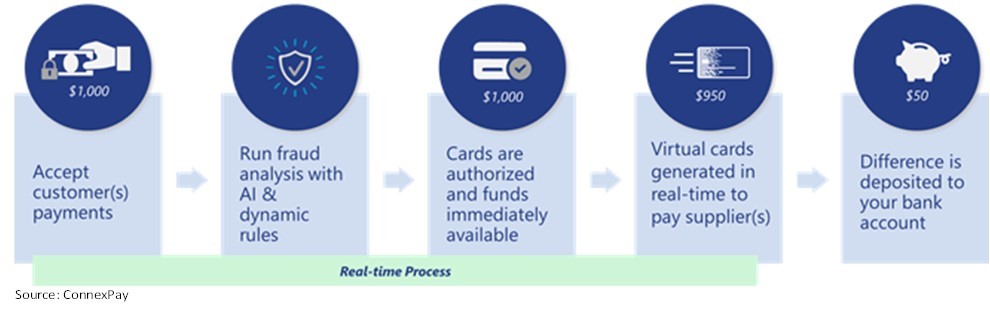

We believe intermediaries are a critical backbone of commerce. Managing payments on behalf of their customers is essential to powering the best customer experience possible. We’re excited to announce our investment in ConnexPay, a company that puts transparency and control of payments back in the hands of these important businesses that own the customer relationship. ConnexPay has built a powerful platform that tackles the infinitely complex problems intermediaries face when it comes to payments — accepting consumer cards, paying suppliers, routing payments intelligently, managing fraud, chargebacks and refunds— and exposes it all with a simple set of APIs. This elegant and truly end-to-end solution empowers intermediaries to facilitate the payment for their customers by becoming the merchant of record with the flip of a switch, thereby improving profitability, reducing fraud, speeding reconciliation, and removing the need for pre-funded accounts and credit lines.

This problem is particularly apparent in the travel industry, where ConnexPay got started. Online and offline travel agents remain an enormous force in travel, processing ~$740B in total global spend each year. Travel is paid for immediately on booking, yet travel agents and OTAs (Online Travel Agents) typically have a one to two day lag awaiting funds settlement from travelers. Further, agents want control over the customer experience, latitude to negotiate supply in advance from suppliers, and the ability to take commission directly out of the payment flow versus reconciling on the back-end with suppliers. ConnexPay solves all of these problems by helping agents become the merchant of record, supported by its unique solution granting instant funds availability.

Illustrative payment flow for an intermediary with ConnexPay:

It’s an elegant solution, and one which we are especially excited about having long searched for disruptive businesses in travel payments. In the same way our planes aren’t flying any faster than when we were kids, payment tech in travel has hardly evolved to the digital world. From our own portfolio, we’ve seen first hand the incredible value of integrated vertical payments solutions (e.g. Toast, Flywire) and the opportunity for technology disruptors in travel and hospitality (e.g. OTA Insight, Avantstay). Our ongoing search for solutions improving the bewildering, complex world of travel payments led us to ConnexPay.

At the outset of the COVID pandemic, we started talking about investments in terms of scratches and scars. Urban exodus: scratch or scar? Work from home: scratch or scar? Time and again, the travel industry has shown resilience coming out of every existential crisis it has faced, man-made or otherwise. Some might believe global travel will never fully recover; we believe our increasingly globalized world is nowhere near the ceiling on tourism and business travel. With the hopeful news of a COVID-19 vaccine, we like many others are dreaming about life when we can travel once again.

While ConnexPay began in travel, its growth during this challenging period for the industry only strengthened our belief in the value of their solution. We’re equally excited the team is demonstrating success beyond the travel sector and into insurance agencies, freight brokers, and e-commerce marketplaces. We’re especially thrilled to be partnering with ConnexPay Founder and CEO, and payments industry veteran, Bob Kauffman, whose leadership roles at US Bank and Elavon propelled the vision for ConnexPay. Bob has attracted a talented team of payments experts, including Jacob, Beth, Julie, Kunal, Judson and many more. Thanks for welcoming F-Prime Capital as part of your story!

Odaseva

Odaseva partners with the largest and most sophisticated organizations in the world to accelerate their trust in business-critical cloud applications. Fortune Global 500 industry leaders use Odaseva technology to back up and restore data, ensure data privacy and regulatory compliance, and use data to drive operational agility. Engineered for Salesforce by Salesforce experts and endorsed by Salesforce Ventures, Odaseva is trusted by 30+ million users and has received 100% five-star reviews over eight years on the Salesforce AppExchange.