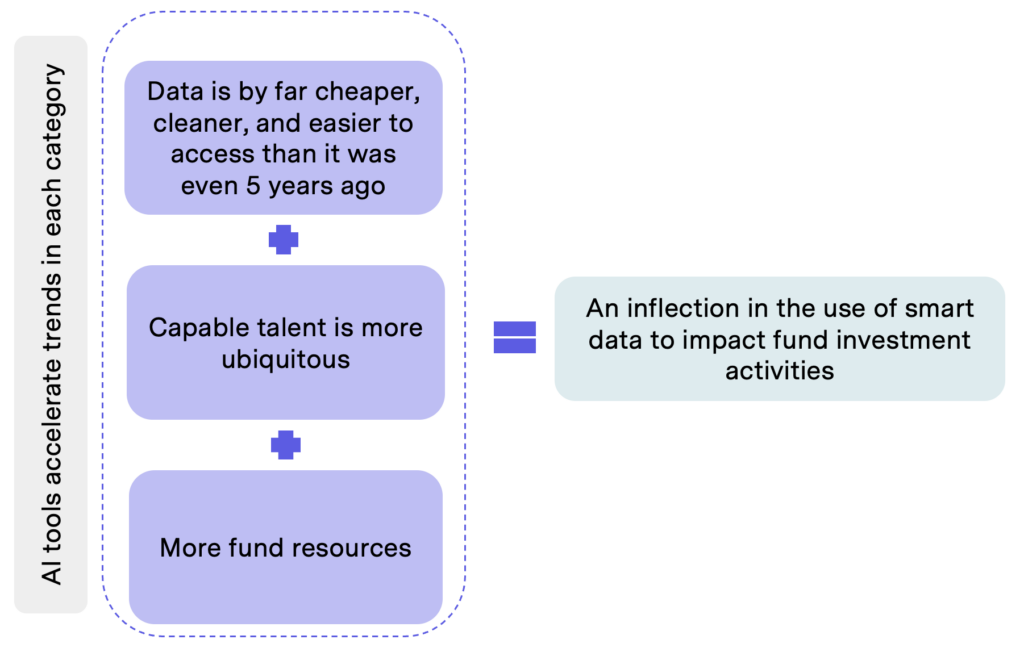

In our previous article, we explored how data in venture capital is reaching a pivotal moment. With various market forces driving more VCs to invest in data efforts, we outlined several key areas where data can be leveraged effectively, and discussed different levels of impact these efforts are having.

To build on that foundation, we conducted a survey among our peers in the industry to understand how they are leveraging data, engineering, and automation, and evaluate the effectiveness of these efforts. This article delves into the survey results to highlight what areas are most important to VCs, where data initiatives have been most impactful, and how firms can interpret these findings to optimize their own strategies.

Survey Insights

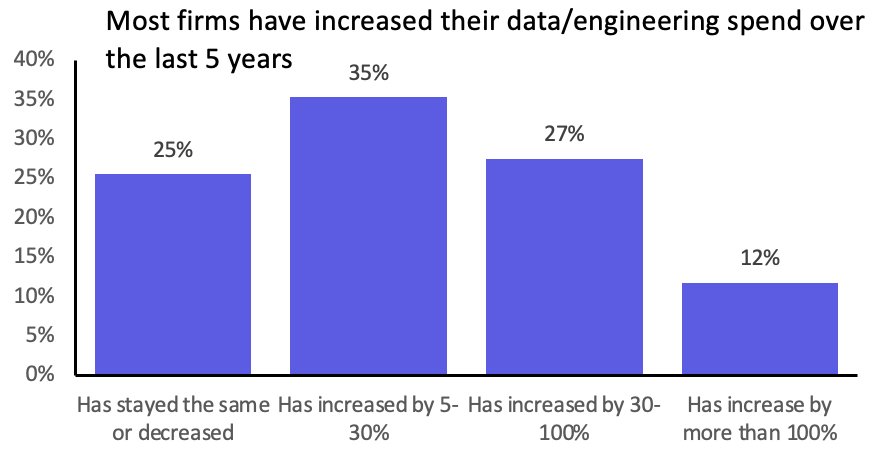

Q1: Have you increased investment in data/engineering over the past 5 years?

The response is clear: 75 percent of the more than 50 firms surveyed have indeed increased their investment in data and engineering in the past five years. This trend aligns with our discussion in the last article about the growing emphasis on data-driven strategies within VC.

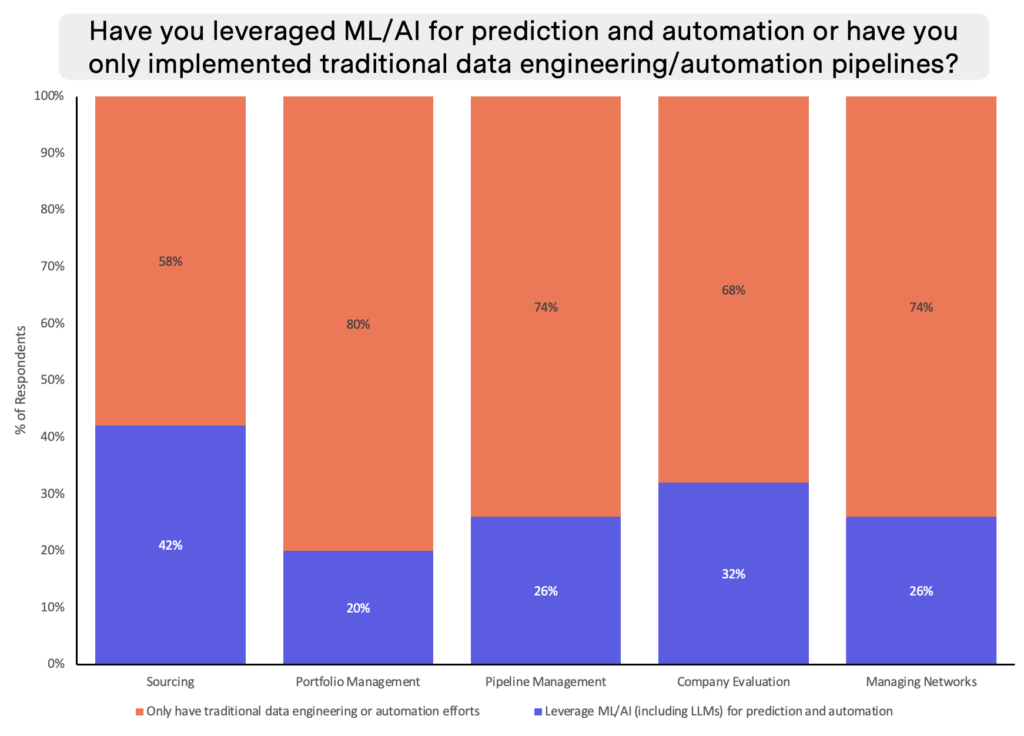

Q2: What are the key areas where you apply data science/engineering, and in what ways do you leverage it?

We asked respondents to categorize their data efforts into the five key areas discussed in our previous article.

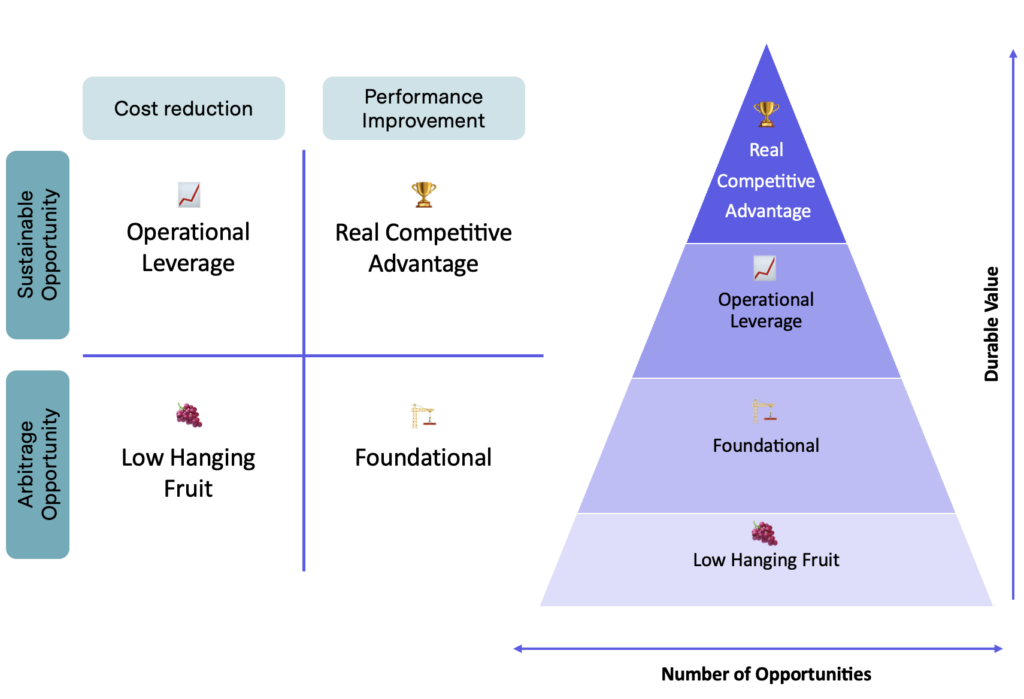

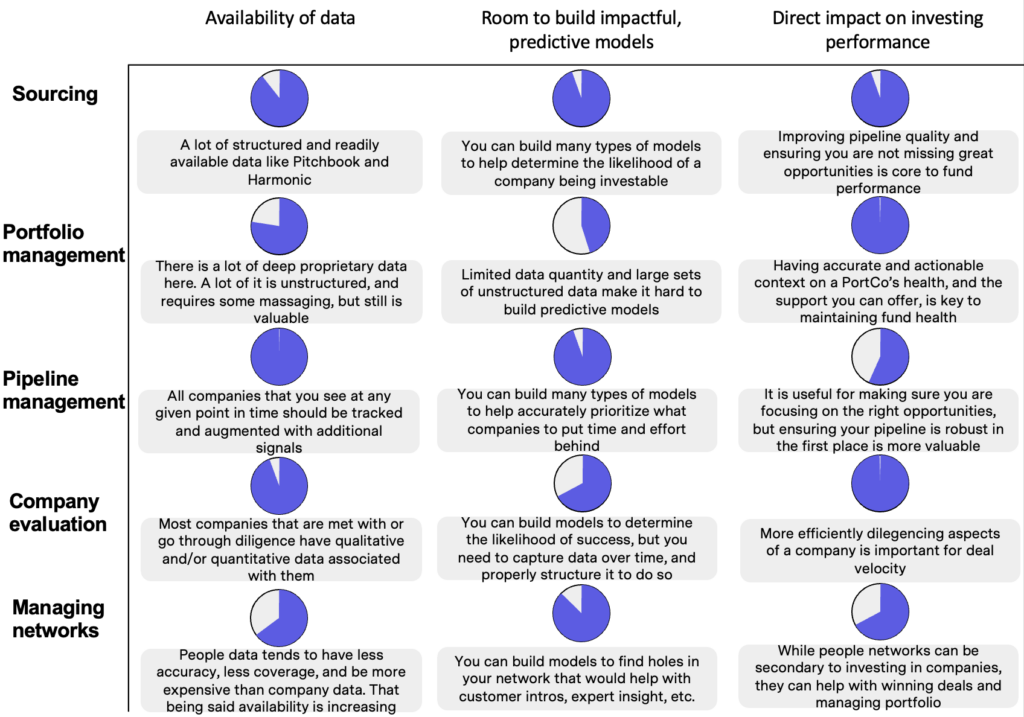

At a high level, the places where people seem to be putting the most effort seem to be those where there is a high availability of data, room to build impactful predictive models, and a clear and direct impact to investing performance. Here are some additional details:

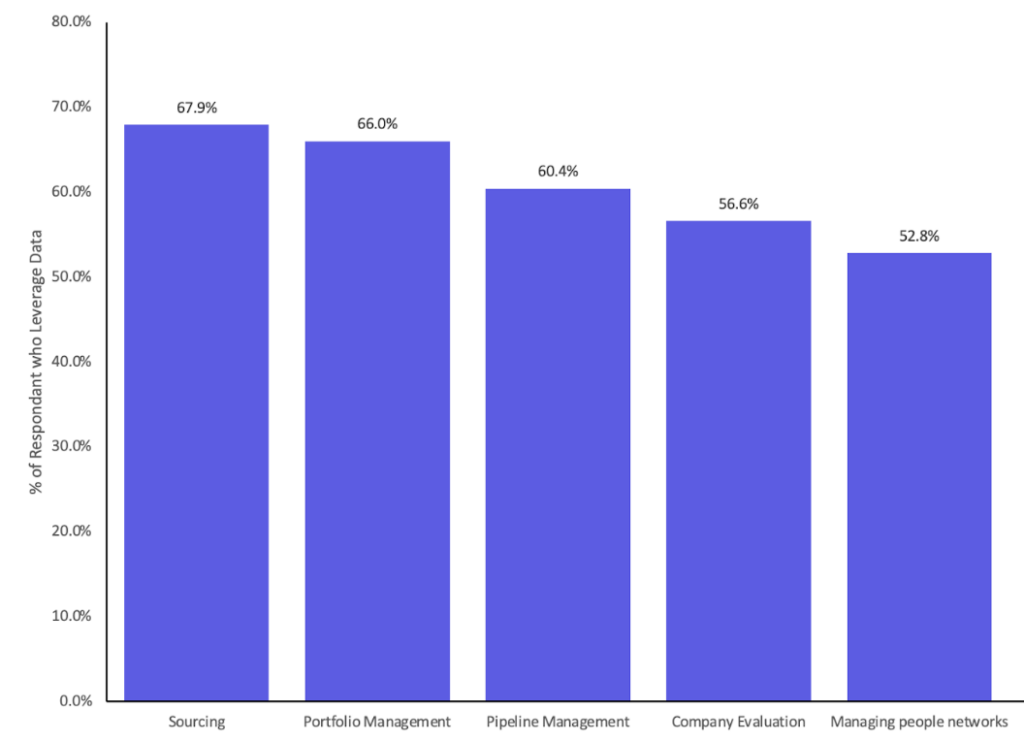

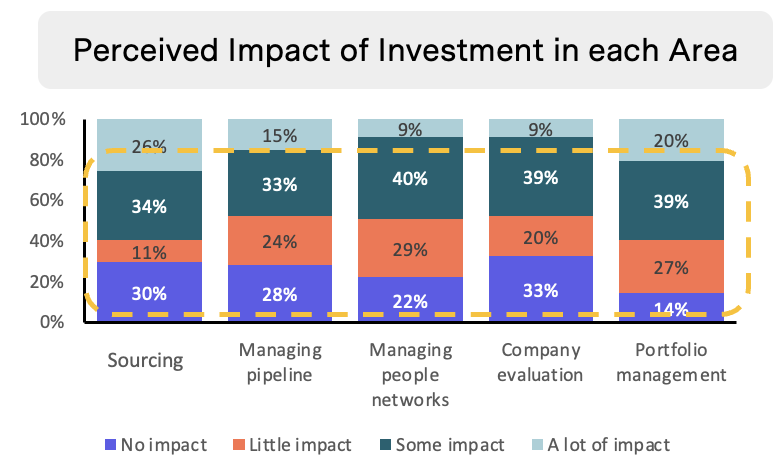

Q3: In what area do you think your data efforts have yielded the most impact and automation?

If you look at the proportion of people who believe their efforts in each area have yielded some or a lot of impact, it more or less correlates to what firms focus on most. Data efforts in “sourcing” and “portfolio management” are perceived as the most impactful, and the rest don’t have as much consistent value. Despite this, only 50 to 60 percent of firms reported achieving meaningful impact from their efforts, suggesting a gap between potential and realized outcomes. Though this looks like an existential crisis for data driven VC, we believe this gap stems from a focus on low-hanging fruit and foundational efforts rather than more impactful, differentiated projects.

Here are some examples of lower level projects vs. those that create differentiated value:

Sourcing

🍇 Low-hanging fruit:Scraping popular public lists of companies

🏆Competitive advantage: Building models to predict the relevance of companies to your firm’s strategies, the likelihood of them responding to a cold outreach, the likelihood of them getting through stages of your pipeline

Portfolio Management

🏗️Foundational: Aggregating portfolio data in a consistent structured format

🏆Competitive advantage: Accurately automating aspects of portfolio support requests (customer requests, hiring requests), modeling portfolio metrics against past and new non-portfolio companies that you meet

Pipeline Management

🍇 Low-hanging fruit: Creating automated email and linkedin campaigns for cold outreach

🏆 Competitive advantage: Consistently reprioritizing your early pipeline based on signals like the likelihood of the company looking to raise soon and fit with your firm’s strategy

Company evaluation

🏗️ Foundational: Organizing all files from companies you meet with and making it queryable

🏆Competitive advantage: Compare the business models, markets, and so on with new companies to similar past companies seen in the pipeline, synthesize an initial analysis of a company based on company files

Managing people networks

🏗️ Foundational: Mapping the experiences and expertise of everyone in your network and being able to search/filter it

🏆Competitive advantage: Proactively finding relevant holes in your network and finding secondary connections to fill them

Automation vs. Impact

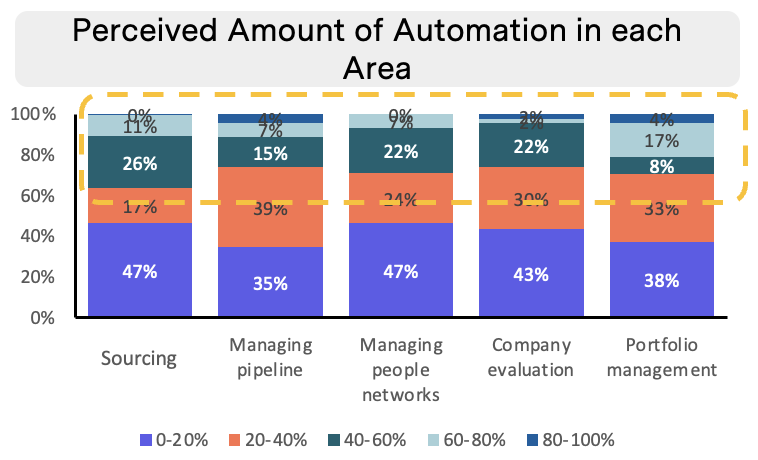

The survey also highlighted automation trends across these areas. Generally, automation levels are relatively low across all domains, with “sourcing” and “portfolio management” seeing the most automation. However, there are key insights to consider:

1. Limits of Automation: There is a cap on how much automation is feasible in any given area. This limitation arises from the complexities involved in obtaining quality data, generating reliable insights, creating valuable outputs, and developing effective workflows. For example, while the potential for automation in “sourcing” is high due to the availability of structured data, areas like “company evaluation,” where data is sparse and unstructured, have lower automation potential.

2. Automation vs. Impact: It’s important to note that automation does not directly equate to impact. Even if an area cannot be fully automated, the impact can still be significant. For instance, “human-in-the-middle” systems, such as research tools that help query past company data, may only automate the information retrieval part of the process but can greatly reduce research effort and prevent the loss of valuable insights.

3. Automation as Low-Hanging Fruit: Currently, most automation efforts fall into the “low-hanging fruit” category, providing immediate efficiency gains. However, as data teams move towards more foundational, operational leverage, and competitive advantage projects, the scope for full automation diminishes, and its direct impact becomes less pronounced. More complex, high-impact efforts often require a balance of automation and human insight while also being more bespoke.

These findings suggest that while automation can offer quick wins, the real value lies in combining automation with strategic, high-impact data efforts that provide long-term differentiation and competitive advantages. As firms mature in their data capabilities, focusing on areas with the greatest potential for sustained impact will be crucial.

The survey results highlight a clear trend: data teams in venture capital are concentrating their efforts in areas with abundant data, opportunities for impactful predictive modeling, and a direct link to enhancing investment performance. This makes sense. However, it’s important to note that despite their efforts, many firms do not perceive much impact. This is likely due to efforts being spent on low-hanging fruit and foundational projects.

But as data capabilities mature, it is important for VC firms to move beyond basic automation and low-impact projects and towards differentiated efforts. Beyond organizing, pulling structured insights, and building predictive mechanisms from external data sources like Harmonic and LinkedIn, this means doing the same for your rich internal datasets like company diligence documents and portfolio company data.

There are dozens of data and AI initiatives you can pursue in each of our core categories, but if you prioritize them in the framework we have described, you’ll be more likely to reap value for your fund. In our next article, we will explore the industry’s expectations for the future of data, engineering, and automation in VC, and how firms can prepare for the next wave of innovation in this space.