Fintech in Q3 — And Loads of New Functionality for the F-Prime Fintech Index!

Fintech in Q3 — And Loads of New Functionality for the F-Prime Fintech Index!

Profitable Fintechs That Demonstrate Sustained High Growth Are Rewarded With Big Multiples in Q3. The Rest — Not So Much.

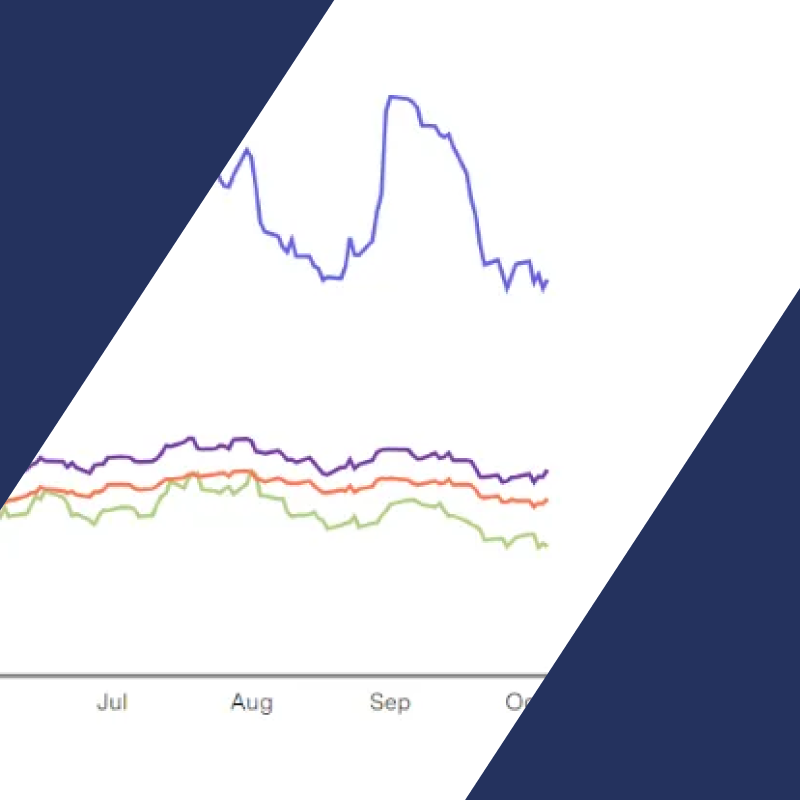

Headline: This quarter, we wanted to show how the Index has performed over the past year. After the significant decline in fintech stocks alongside the broader tech sector in 2021 and 2022, fintech disruptors have quietly recovered a lot of ground over the last twelve months. The F-Prime Fintech Index is up 80%+ LTM, though still ~60% off its 2021 highs. The F-Prime Fintech Index continues to outperform other indexes we’re tracking: the Emerging Cloud Index was up ~6%, Nasdaq grew ~27%, and the S&P 500 climbed ~19% over the past year.

Despite a year-to-date rebound, the F-Prime Fintech Index lost $74B in market cap in Q3, with the median market cap decreasing from $2.8B to $2.4B. Payments companies Adyen, Shopify, and Block drove 75% of the decline, losing $31B, $13B, and $13B respectively in market capitalization in the wake of earnings and profitability misses, plus headwinds in the overall market.

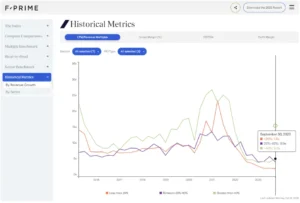

Multiples: Companies that continue to grow rapidly (that is, 40%+ YoY) have seen an increase in multiples to 5x, up from 3.8x last quarter. Investors are rewarding sustained high-growth with higher multiples — a reversion to historical valuations and a change from our last update. For the first time since Q4 2021, high-growth companies are garnering higher multiples than medium growth companies (see the flip in the chart above), despite the fact that most have not achieved profitability.

However, most high-growth companies are still trading significantly below their 2021 multiples, on average reaching ~40% of their Q4 2021 multiples. A few companies have nonetheless exceeded their 2021 multiples, rewarded for their sustained high growth and profitability. Well done, Wise — 72% YoY growth and 12% profit margins.

By sub-sector: Sectors that experienced significant valuation re-ratings in 2022 saw the biggest bounce back in Q3. Multiples in the lending vertical rebounded from 1.1x in Q4 2022 to 6.1x this quarter. Category leader Affirm increased to 6.8x from 3.7x; however, removing Funding Circle from the Index and Lufax’s lack of multiples (due to its negative enterprise value) account for ~50% of the increase in average lending multiples.

Macro and real-estate sector concerns continue to weigh on the proptech vertical which is still trading at ~1x, though better than 0.5x at the beginning of the year. Meanwhile, all proptech companies in the F-Prime Fintech Index saw multiples increase, with Blend seeing a jump to 2x from 0.8x.

While the durability of payments businesses has garnered stable multiples (4.5x for the past year), a few — Shopify, Flywire, Mercado Libre, Remitly, and Wise — have seen improvements in multiples. Likewise, B2B SaaS companies have continued to attain the highest multiples (more details below).

Index removals: While M&A activity continues to increase in both public and private markets, no F-Prime Fintech Index companies were acquired this quarter. However, Bright Health Group (BHG) no longer met our criteria and was removed from the Index.